The following reflects personal views of the author as of the publication date and is not intended as investment advice or a description of any investment strategy or performance. Opinions may change and should not be relied upon for investment decisions.

There is a common (and fair) view that specialization is important for generating alpha within largely efficient public markets. The view is generally that investors must focus on a niche – whether a specific sector, region, or market cap – to gain an analytical edge. For example, allocators might seek out a European mid-cap specialist or a biotech-only fund, trusting that deep domain expertise in a narrow universe can beat broad indices and allow for differentiated returns. This mindset seems to stem from the efficient market hypothesis: if markets rapidly price in information, only a highly focused specialist operating off the beaten path might exploit minor inefficiencies.

But there is another type of specialty – so rarely acknowledged today that it has become a hidden specialty – that focuses its efforts on the areas of public markets that have historically produced the strongest long-term returns. Over the last century, the bulk of stock market wealth has not come from broad market efficiency or sector rotation; it has come from a tiny fraction of extraordinary companies that cut across different sectors and geographies.

Research by Hendrik Bessembinder famously showed that just 4% of U.S. listed companies accounted for the entire net wealth created in the stock market since 1926. In global markets from 1990–2020, an even smaller cohort – only about 2.4% of companies – accounted for all net stock market gains beyond Treasury bills.

These facts should reframe what “skill” in stock picking truly means. The ultimate specialization is the ability to consistently and repeatedly identify and invest in those few truly exceptional businesses that end up driving the majority of wealth creation. We believe this is the most important specialty of all, but one that has been largely overlooked. There are several reasons for this that we explore. One interesting reason is the difficulty in explaining this type of specialization to those who do not have it. There is very much a “you can’t fully appreciate it unless you’ve lived it” aspect to this specialization. In other words, it is a difficult specialty to market and much less conducive to good storytelling than traditional specialties. Its waning popularity has caused many who could become skilled practitioners in this area to look elsewhere. It is not lost on us that the very specialization that can best position investors to consistently identify the types of businesses that have produced the strongest returns, and with the longest duration, has only become less competitive over time.

Traditional Notions of Specialization

In traditional terms, a “specialist” investor is defined by scope of coverage. This usually means constraining the investment universe by region, sector, or strategy:

- Geographic or Regional Specialists: Investors might focus on only Japanese equities, emerging markets, or frontier countries like Turkey and Thailand. The premise is that local insight and on-the-ground knowledge within areas that aren’t as “well covered” by others can create an informational or analytical edge where others are less informed.

- Sector Specialists: Many investors carve out niches in industries such as healthcare, semiconductors, or biotech. A biotech specialist, for example, is expected to understand drug pipelines and FDA approval probabilities better than others – turning that expertise that only a smaller group has into alpha.

- Market Cap or Style Specialists: Some focus only on small-caps or micro-caps or even something like European mid-caps, with the idea being that these specialists are uncovering gems that investors focused on larger companies overlook, while others might specialize in areas like distressed debt.

These traditional specialties indeed narrow an investor’s universe, often to around 150-300 companies, and allow the investor to demonstrate deep focus and domain expertise around this group that they get to know intimately. For perspective, the MSCI Europe Mid Cap Index contains 220 constituents – on the same order of magnitude as many sector-focused stock universes. The intuition is clear: by limiting their scope, specialists can go deeper on each company, demonstrate analytical edge, and act faster than those with broader coverage.

There’s evidence that sector-specialist funds have proliferated and often outnumber “generalists,” as allocators currently seek targeted expertise. For example, one recent analysis noted that “the new frontier for alpha is found in niche strategies” where deep, focused knowledge lets investors find mispriced assets. In practice, a skilled semiconductor analyst might leverage industry contacts and technical understanding to anticipate a chip shortage, or a biotech-only investor might better assess the probability that a Phase 2 drug candidate will ultimately get FDA approval. Many allocators naturally gravitate to these types of specialists, believing that’s how one beats an efficient market – by knowing more than anyone else about a very specific domain that produces clear winners, losers, and everything in between.

However, this common view of specialization misses a critical point: it focuses on where an investor looks (e.g. which sector or region), rather than what they are looking for. Yet decades of market history suggest the “what” is important, leading to incomplete specialization definitions today. Alpha has not been evenly distributed across common areas of specialization. Instead, it has concentrated in an exceedingly small subset of truly exceptional companies. Understanding this concentration of wealth creation is important for understanding why the conventional idea of specialization needs an update.

A Few Companies Drive the Majority of Returns

Public market returns follow a power-law distribution. Most stocks are mediocre or worse, and only a tiny minority are responsible for virtually all the market’s wealth generation. Bessembinder’s research quantified this skew in stark terms:

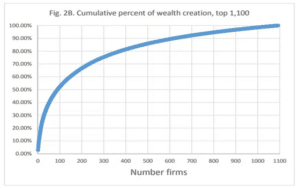

- From 1926–2016, just 4% of U.S. stocks (around 1,000 companies out of ~26,000) accounted for all net stock market gains, with the other 96% of stocks collectively just matching short-term Treasury bills. Almost every stock was a loser relative to risk-free T-bills, except for the few big winners. The top 90 stocks (a mere 0.3% of the total) delivered over half of all wealth creation.

- Globally, the pattern is even more extreme. Between 1990–2020, only 1.5%–2.4% of worldwide listed companies (roughly 1,500 out of ~64,000) generated 100% of net global wealth creation. The other 98% collectively added no value above Treasury rates. In fact, more than half of global stocks during that period lost money in absolute terms.

Figure: Cumulative share of total stock market wealth creation by top-performing companies. A small number of big winners (rightmost tail) accounts for essentially all long-term wealth creation. In the U.S., the top ~4% of firms generated the entire net gain since 1926. Globally, just ~2% of companies did the same from 1990–2020.

The implication is that alpha in public markets has largely meant owning those few “superstar,” or “elite compounder” companies, not broadly outperforming within a sector or region. As one investment commentary summarized, more than half of stocks underperform even cash, while “a tiny minority of exceptional growth companies generated the bulk of stock market returns.”

The ultimate skill is a combination of stock selection and sizing – but not just any stock selection. It is the skill of picking out the potential 2-4% of companies that become the big long-term compounders, and crucially, having the conviction and structure to hold them (likely with varying position sizes) through years of compounding.

Contrast this with the traditional sector specialist’s goal. A chemicals-sector fund, for example, might aim to beat the chemicals index by a few percentage points through superior analysis of supply/demand cycles. That is a worthy objective, but even if achieved, it pales next to what the true outliers have delivered over time. And we would argue that the increased activity and timing elements that these types of strategies usually introduce increase the likelihood of errors of commission and the overall complexity factor. Consider that just a handful of companies like ExxonMobil, Apple, and Microsoft have accounted for 10% of all U.S. stock market wealth creation in the last century. Being invested in even one of these mega-winners in a meaningful way can produce more absolute alpha than years of middling outperformance in a narrow peer group. The same is true globally – the top five global stocks (recently including names like Apple and Amazon) accounted for over 10% of ~$75 trillion in wealth created since 1990.

In effect, markets are efficient most of the time for most stocks but typically inefficient over the long term, and profoundly inefficient during certain periods of market fear along the way, in pricing the rare companies that go on to lead and reshape industries and markets. These companies often begin as seemingly expensive, controversial, or niche themselves, which is why so many investors often underappreciate them through many years of their public lives. It is precisely here, in the identification of future leading businesses, that an investor can add the most value through applying a combination of analytical, behavioral, and structural edge. Bessembinder himself notes that if an investor “has a comparative advantage in identifying in advance the stocks that will generate extreme positive returns,” the gains from stock selection can be enormous. The challenge, of course, is developing that comparative advantage, which is a different – but real – specialization.

Defining the Hidden Specialist: The Elite Compounder Specialist

What do we call an investor whose coverage universe includes the most likely next generation of Fortune 100 companies, along with current Fortune 100s that have an ability to become Fortune 10s or the Fortune 1? This coverage universe is not defined by traditional sector, company size, or geography boundaries. It is defined by the “what”: primarily the nature and magnitude of the competitive advantage, market opportunity, product development and innovation capabilities, and management quality, along with a deep understanding of the types of mispricing events that can occur around these businesses. We call investors who become unusually skilled in this type of assessment elite compounder specialists. It is a specialty of analysis, behavior, discipline, and structure rather than of industry or geographical silo. Let’s define the specialization’s characteristics:

- Deep Focus on the Intersection of Strongest Competitive Advantages, Large Market Opportunities, and Operational Excellence: The investable universe is limited to companies that show evidence of having the strongest competitive advantages, long growth runways, and superb management. As is the case with widely recognized specialties like semiconductor analysts, dispersion is wide across those who claim to be specialists in this area and those who actually are. However, unlike semiconductor specialists, the dispersion within this specialty is widely misunderstood. For both types of specialists, it is initially difficult for an outsider to determine whether the specialist is one of the few “good apples.” However, storytelling suffers much more in this area of specialty, which has caused even the good apples to be misclassified as “global generalists lacking a clear area of expertise.” For example, semiconductor specialists do a great job of almost instantly making the listener feel like they are talking to an expert. Industry jargon like DRAM, HBM, advanced packaging, CoWoS, detailed discussions about logic chip supply/demand imbalances, etc. is typically sprayed everywhere during discussions with these specialists in a way that can make it easy for the listener to conclude that there is a knowledge base here that (1) the listener knows he or she doesn’t possess and feels he or she cannot easily obtain, and (2) the listener feels not many others seem to possess based on their experience and prior discussions. In other words, there is complexity bias that more naturally allows those who are more commonly classified as specialists to be considered true experts. But for elite compounder specialists, it is quite the opposite. The “jargon” consists of investors sharing terms and knowledge that the listener has likely heard many times before and that the listener often “feels” can be easily obtained. This allows so many investors, across the good apples and bad alike, to sound very similar to one another, even though what they actually do, where they have been, how they actually invest, and how they go through their respective processes vary significantly. So, discussions with elite compounder specialists often result in widespread apathy and often boil down to some version of, “Oh, another investor claiming to have an edge in investing in great businesses that we’ve all heard of before.” This is the very view that is need of massive updating, but at the same time, creates the opportunity. In fact, in our experience, those with true expertise in the key areas of the elite compounder specialty like not just understanding competitive advantages like network effects, but understanding their strongest variants like those that also come with data and infrastructure advantages, and the type of management that is required to appropriately balance key stakeholder interests over long periods of time in the face of almost endless growth opportunities and business volatility are among the rarest specialists in public markets. In practice, those who are highly trained and skilled in finding the intersection of strongest competitive advantages and large market opportunity will maintain a coverage list of only a few hundred companies globally max (often ~250 or fewer at any given time that might meet the strict criteria). This is often a smaller coverage universe than that of many sector specialists. For perspective, a dedicated mid-cap Europe manager might follow ~200+ companies, and a global healthcare fund easily has thousands of listed companies to consider. The elite compounder specialist, when done right, is a dogged hunter both for companies they already know well but do not quite (but could) meet the required criteria and for companies they haven’t followed as closely to date that could be strengthening. The elite compounder specialist, when done right, passes on 99% of stocks though, and passes on most of them fairly quickly, while demonstrating an unusual ability to zero in on the elite few that could appreciate by multiples over the next decades (across all sectors) more efficiently and precisely than others. In that sense, this approach is even more specialized (in the rarity of companies targeted) than a typical niche strategy. It is a narrow quality filter (rather than a narrow industry or geography filter) that in our experience requires 30,000+ hours of dedicated focus and hundreds of company reps to develop the right heuristics and pattern recognition (it is not just about time served; it is also about cycle and situational experience).

- Cross-Disciplinary Expertise: Because elite compounders can emerge in any sector or country, the investor must be broad in capability but ultra-discriminating in standards. This is not generalism in the usual sense (it’s not owning “a bit of everything”). Rather, it requires multiple domain knowledges within one brain – for tech, healthcare, consumer, etc. – all applied through the lens of identifying top-tier competitive advantage and utilizing the cumulative knowledge and proprietary heuristics developed to be better positioned to analyze the next potential elite compounder and potential mispricing setups around it. In practice, the research process is its own specialty: it involves understanding several different types of competitive advantages, that can all vary in type and magnitude, including network effects, scale, customer, supplier, or talent captivity, intellectual property, cultural moats, regulatory barriers, brand affinity, and other sources of insulation from competitive disruption. An investor that aims to back only next Fortune 100s, for example, might assess a software company one month and a medical devices company the next, but in each case the investor is looking for the same rare hallmarks of greatness that have been refined and curated across a career’s worth of work that has been focused only on this mission. This requires a framework for and heuristics around business quality that is based on lived experience and transcends sector silos. And it requires a careful balance that only this type of specialist possesses of going deep enough across multiple domains to have the knowledge required to exercise winning judgment in most scenarios, while not going so deep that you end up burning precious time on research that is not critical to the investment case but prevents you from covering all the ground you need to for repeatedly identifying next opportunities and further deepening expertise across the critical areas of the approach.

- Behavioral and Structural Edge, and Long-Term Horizon: Perhaps most importantly, this specialization demands a behavior and structure that sets it apart from most others. The skilled investor within this specialty must be willing to run a concentrated portfolio, often with 10–25 holdings but sometimes as few as five if that is what the research process yields. The elite compounder specialist must have experience in holding winners (albeit with varying position sizes) for years to reap the full power of compounding. That means having the firm structure to resist short-term pressure and the proverbial tap on the shoulder during challenging performance periods – an aspect of specialization that is seldom discussed. Many sector funds and other types of specialists are judged on 12-month or even monthly absolute and relative performance; an elite compounder-focused fund must be judged over 5-10+ year periods instead. Investors focused on this must have the temperament and experience to appreciate that winning long-term often requires a large capacity to suffer and staying the course even when there’s no near-term visibility into when the stock will “work,” while at the same time avoiding stubbornness. This balance needs continual refinement and requires a career’s worth of training and deep expertise around human bias and emotion and the defining attributes of the underlying businesses that will determine whether they should continue to grow longer-term despite the shorter-term issues that are causing most others to vote differently. And there must be enough discipline to resist growth temptations and cap capacity for the strategy at $2-3 billion forever to maintain the required flexibility. The elite compounder specialist effectively practices a behaviorally tortuous version of “private equity mindset” where your holdings are marked to market every day and where the structure of the market around you causes way more volatility, leads to way more skepticism around many of your holdings when these positions are going against you, and flat out makes you look stupid not so infrequently. Day-to-day, this type of specialist requires the mental fortitude to be comfortable with feeling inadequate across multiple dimensions. For example, you will often read, learn, and assess certain companies for weeks or months only to conclude that the best action is continued inaction. You will go through extended periods when your positions and portfolio swing much more due to market movements than based on company-specific news or developments that are relevant to your thesis. You will realize that many of the efforts that most others in the industry spend significant time on like traveling for industry conferences and events, management meetings, and regular team meetings can make it feel like you are doing something different and heavier than others but eventually starts to add almost no value as compared to more traditional, in-office research. If done right, this leads to regular feelings of, “Am I doing enough?” or “Don’t I need to be flying somewhere or meeting with someone, now, to justify my existence and fees?” Structurally, this specialty also requires client / LP buy-in to weather volatility and real down years, and a very low percentage of LPs (and investors) have the capacity to suffer through extended periods of weak performance. For example, even the best long-term compounders have gut-wrenching drawdowns: Apple’s stock fell well over 50% on two separate occasions over the last few decades and yet went on to create over $3 trillion in wealth. Amazon famously lost 90% of its value in the early 2000s crash (and dropped precipitously again in 2022), only to become one of history’s greatest stocks. An elite compounder specialist absolutely must have the conviction (and ideally a mandate from investors) to hold through these storms when their research continues to support the investment thesis. Of course, the investment process adds structure and a system that is designed to reduce sizing during periods when expected returns might drop below your cost of capital (or to exit when expected returns are substantially below your cost of capital), but these big drawdowns often occur during periods when valuation is not currently a concern and when expected returns remain satisfactory prior to the event(s) that cause the next drawdowns. As Bessembinder put it, “big drawdowns are the price to pay for superior long-term investment returns.” And as Charlie Munger said, if you can’t handle a 50% market decline with equanimity, you aren’t fit to be a common shareholder and deserve mediocre results. The payoff for developing the required behavioral and structural aspects within this specialization can be significant – Apple’s recovery from those drawdowns, for example, made it the top global wealth creator from 1990–2020. Based on our firsthand experience, including leadership roles at a firm that grew from small to very large, an allocator considering this type of approach should ensure the investor’s behavioral make-up and incentives and firm structure and size enable unusual patience, flexibility, and pure best ideas decision-making because it is exceedingly rare to find but critical for long-term performance.

In summary, the elite compounder specialization is defined by what is targeted (extreme outlier businesses), when they are targeted (documented mispricing framework based on lived experience), and how the investor operates (with extreme patience, discipline, focus, flexibility, and alignment), rather than by a narrow market niche. This is a fundamentally different axis of specialization. It has been “lost” in the classification sense because (1) too many investors have claimed to have this type of specialty over the years, hiding the rarity of skilled practitioners in this area, (2) it is much more difficult for outsiders to “feel” the different aspects of this specialty as compared to others commonly classified as such, and (3) traditional frameworks don’t list “strongest competitive advantage” as a sector or “elite compounders” as an asset class – but they arguably should.

The nuances and complexities involved with this specialty, and how the common perceptions differ versus widely accepted specialties, can be like comparing a Formula 1 engine mechanic to an expert in hiring industry leading talent. People instantly defer and accept that the Formula 1 engine mechanic is a specialist because the difficulty is visible and technical. But when someone says they specialize in hiring industry leading talent, it often fails to land for the listener because so many people have hired, interviewed, managed, or feel they know “what a great hire looks like,” so they assume it’s easier and common. But in reality, most companies are mediocre at hiring incredible people even after decades, the difference between doing this exceedingly well and not can be nuanced and context-dependent, feedback loops can be long and noisy, the cost of small errors can compound significantly, and true excellence requires deep pattern recognition and heuristics across many roles, cultures, and failure modes. “Hiring industry leading talent” feels everyday and familiar, yet top-tier performance is demonstrably rare in this area even among people who focus only on this for a living.

What Makes an Elite Compounder: Key Traits and Examples

Identifying elite compounders requires evaluating qualitative and quantitative factors that signal enduring, strongest competitive advantage and multi-decade growth potential. After 30,000+ hours of dedicated idea generation efforts, research, global travel, mistake-making, and observing these investment candidates and their management in the wild across different market environments, a skilled specialist in this area develops a framework for repeatable outcomes. The foundation of this framework involves proprietary heuristics and a pattern recognition toolkit based on lived experience. For the skilled specialist, it results in consistently (1) identifying elite compounders, and (2) achieving the delicate balance of leaning into volatility when the inevitable obstacles surface while at the same time avoiding stubbornness when the inevitable mistakes or lower probability outcomes surface. Some of the key traits of elite compounders worthy of portfolio inclusion are:

- Leading Customer Experiences: Elite compounders wow their customers by doing something meaningfully different than the status quo. Large groups of people will only spend their precious time and money if the business can add significant quality, convenience, and/or affordability as compared to alternatives. Specialists in this area recognize the potential long-term benefits from backing one-of-one value propositions as opposed to even “strong” customer experiences but ones that 3-5 other companies also provide in similar ways. Here, the specialist serves as an anthropologist of sorts, setting aside his or her personal views and moral compass and instead understanding what other groups of millions to billions of people value and why. Importantly, this can involve backing companies whose businesses have significant negative consequences if the conclusion is the societal harm is an inevitable consequence of a product or service that has been deemed necessary or highly desired by large groups of the population, and that these behaviors are highly unlikely to change so long as the company can recognize, acknowledge, and make progress on mitigating these negative consequences over time. “Wow” customer experiences can be tricky to identify. Sometimes exciting technology and products as of a moment in time like beepers, Blackberries, and Segways prove to be fads or highly disruptable. Other times, products or services that are far outside of the investors’ interests like mobile games or high-end beauty products or cosmetics prove to be durable wants for large segments of the population. Through studying hundreds, if not thousands, of different products and services and different consumer behaviors and habits, the specialist can consistently separate durable wow customer experiences from everything else including fads and trends through demonstrating a top tier understanding for the views and interests of large segments of the population across different countries and cultures.

- Strongest Competitive Advantages: A wow customer experience exists as of a moment in time. Moats can allow wow customer experiences to endure over decades. Not just any moat, but among the strongest and most durable that we have identified to date. These can take many forms – network effects, cost leadership at scale, captive customers, suppliers, and talent, intellectual property, brand power, data advantages, and others. Elite compounders almost always possess a combination thereof and the strongest variants within each. For example, hundreds of companies from Pinterest, to Snap, to Meta, to Reddit, to Airbnb, to Amazon, to Sea Limited, to Tencent, to Roblox, to JD.com have some form of network effects, but specialists in this area have the expertise required to filter carefully for the strongest network effects variations with an awareness that reaching these highest levels is necessary for both proper risk management on the way in and satisfactory long-term compounding. Sticking with the network effects example, Amazon has stood out over the last 15+ years. Its rare competitive strength isn’t due to simple network effects alone (more buyers attracting more sellers and vice versa), but network effects coupled with a proprietary data advantage and a massive infrastructure moat, plus differentiated scale across more than one business line. Network effects can come undone nearly as quickly as they can strengthen, so identifying the strongest network effect variants is important for lowering risk of permanent loss of capital events and for increasing the probability of satisfactory investment returns with duration. Consistently identifying these types of multi-layered moats – what one investor dubbed a “lollapalooza moat” of many advantages working in concert – is a key part of the elite compounder specialist’s skillset. A generalist who lacks the right tools might have seen Amazon in the 2007-2012 era as just an online retailer (low-margin, overvalued); the compounder specialist saw a network/data/infrastructure juggernaut in the making, worth backing for the long haul. On the flipside, a generalist who lacks the right tools might view Pinterest or Zillow as businesses with good enough competitive advantages that are “too cheap for what they are”; the elite compounder specialist would classify them as intriguing companies worth watching with curiosity and open-mindedness, but with the discipline to remain on the sidelines even when valuations are optically low for so long as the conclusion is their network effect variants are too weak to justify taking significant time away from further study of and investment in the smaller group of businesses that either already have, or are much better positioned to, achieve elite compounder status.

- Large and Expanding Addressable Markets: Elite compounders must be able to grow well above GDP for decades, ideally by expanding their product portfolios or entering new markets (“Act II” and “Act III” opportunities). For these companies, their growth serves as both a margin of safety and the source of share price appreciation. One (even very large) product alone usually puts an unacceptably low ceiling on compounding. The specialist therefore studies the types of companies, managements, and situations that should reasonably allow for product extensions and adjacencies (businesses and geographies) where it has a right to win rather than some ability to simply “take just enough market share within a large market.” Alphabet (Google) illustrates this well. Google started with search, which itself was a large market with strong network effects (more users → more data to refine search algorithms → better results → more users – a self-reinforcing loop). But Google was able to move into online advertising technology and tools (AdSense / AdWords), mobile operating systems (Android), public cloud computing (GCP), user-generated video content (YouTube), generative AI (DeepMind, Gemini), driverless cars (Waymo), and more – through leveraging its scale, core data, and engineering prowess. Importantly, Google’s core competitive advantage (its algorithms and data leadership in search) proved transferable into other areas. An elite compounder specialist in the 2007-2014 era, particularly during periods of controversy like the PC to mobile transition and then the mobile browser to mobile app transition, would have noted not only Google’s ~90% search market share but also many of the reasons behind it including the ways in which consumer habits hardened in this area and the winners-take-most nature of this market, along with Google’s relentless R&D and ambition to “organize the world’s information,” indicating a long runway beyond just desktop search. The commitment to and execution on innovation and continual product improvement is another common thread: elite compounders typically invest heavily in R&D while still achieving superior growth and profitability over longer periods through demonstrating high R&D productivity as well. That willingness to plow capital into new initiatives (think Google’s “moonshots” or Amazon’s AWS buildout), plus the management, talent, and overall positioning to find success in certain of these areas, often separates those that end up becoming part of this small group of next Fortune 100s from the many more that might look the part for a period but ultimately fail to withstand the test of time. Consistently identifying these dynamics goes well beyond “looking for big end markets,” which is commonly talked about in ways that dilute the importance of this aspect of the work. Instead, it requires close study of many of these situations over long periods of time as their businesses evolve and new opportunities and threats emerge, along with close study of – and in some cases directly participating in – those that seemed to have similar opportunities but weren’t able to fully capitalize like Peloton, DocuSign, Snap, and Lululemon. As the specialty deepens over time, eventually the required discerning filter in this area sufficiently strengthens, allowing the specialist to carefully narrow to the much smaller group that proves to address large and expanding addressable markets over multi-decade periods.

- Exceptional, Often Founder-Led Management: It’s no coincidence that many of the elite compounders have founders at the helm for many years post IPO who are not only visionaries but also prove to be excellent strategists and operators. Founder-led companies have been shown to outperform, in part because they tend to be more innovative and willing to make bold but rational and thoughtful long-term bets. But being founder-led is not always required. It is also important to recognize that certain others are founder-like with respect to their skillsets, drive, and alignment. The skilled elite compounder specialist assesses leadership quality closely, again guided by heuristics and pattern recognition built over the course of one’s career. It involves understanding what great track records of capital allocation look like, identifying the connections to their mission-driven approach, assessing whether they foster a high performance, high accountability culture that can sustain today’s competitive advantages, and whether they have that unusual, relentless intensity and competitiveness that can keep the company’s mission as the top priority even after achieving massive success. For example, UnitedHealth Group may not have had the same household-name leadership as certain tech firms and didn’t have a true founder at the helm during much of its history. But its leadership over decades, namely Stephen Hemsley, built a different type of integrated health insurance and health provider network in the U.S. by first having the vision for why this was important and then continually adapting over a multi-decade period. Adaptation and product improvement has occurred across multiple dimensions – from insurance underwriting operations (UnitedHealthcare) to its full-blown diversified health services provider (Optum). UnitedHealth’s management understood both how to achieve scale (now over $300 billion in revenue) and how to better integrate vertically to improve healthcare outcomes and grow. They acquired physician groups, pharmacy benefit managers, outpatient surgical centers, in-home care providers, and data analytics firms, bolstering the network effects within its health insurance business in similar ways to certain tech firms. For example, adding data from clinical operations to better inform insurance and vice versa. The ability of management to execute on such a vision – essentially reinventing the business multiple times, particularly when Hemsley recognized the importance of adopting a much more integrated model than was traditionally accepted at the time – is a hallmark of an elite compounder. There is well-known principle that some of the best businesses do not require the best management, but skilled specialists in this area recognize that the small group that has driven all the value in public markets typically checks all the important boxes, including unusually capable leadership.

- Documented Mispricing Events: The elite compounder specialist is attuned to recurring mispricing patterns in public markets that create entry or sizing opportunities in these businesses. Contrary to the widespread but misguided notion that “everyone knows most of these are great companies,” history shows that even the best stocks go through periods – and usually more than one – of apathy, skepticism, or full-on controversy. Sometimes the entire market cycle provides the opportunity (e.g., the tech crash of 2000-2002, when Amazon, Apple, etc., were left for dead by many, or the 2022 post-Covid / inflation tech drawdown when Amazon, Netflix, etc. saw their share prices decline by 40-70%). Other times, market structure, company-specific, or other behavioral issues create the opportunity. It can be driven by a short-term earnings “miss,” a product or capital allocation misstep, unexpected cyclicality, interesting new competition, management turnover, a data or security breach, or several other reasons. The specialist doesn’t always get this right by any means but is able to repeatedly separate the temporary setbacks and buying opportunities from true structural issues that present unacceptable risk of permanent loss of capital. For example, both Alphabet and Meta faced antitrust investigations, advertiser boycotts, and moat attacks in past years that dented the stocks on multiple occasions; the specialist is able to consistently look through what proves to be transient issues to the robustness of Google’s and Meta’s businesses mainly due to the unusual difficulties in taking significant share from their core offerings over extended periods. Likewise, UnitedHealth has seen its stock valued well-below market multiples for much of its history due to political rhetoric, regulatory uncertainty and changes, and low NPS scores and negative headlines in certain areas due to some of the unfortunate realities of U.S. healthcare – yet over time it has consistently demonstrated that it is a flawed but critical component of the also flawed but critical U.S. healthcare system in a way that has allowed it to continue growing revenues and earnings per share at a high-single digit and low-to-mid teens pace, respectively, with healthy returns on invested capital despite having only single-digit operating margins. The key is developing high conviction in the long-term thesis around enough of these businesses globally while having a deep understanding for the types of mispricing events that commonly surface. This provides an analytical framework for identifying when these unusually strong businesses remain fundamentally on track long-term despite short-term issues that are causing the stock to suggest otherwise. This discipline, paired with an aligned capital base that refrains from tapping the specialist on the shoulder when turbulence hits, allows the specialist to endure multiple periods of looking stupid and to add to positions in these scenarios when the market misprices elite compounders due to real but highly likely temporary fears. These repeatable mispricing events (we have identified seven of them to date, but they are generally driven by what we might call the “behavioral gap” – the market’s tendency to underestimate the duration of growth or overreact to near-term setbacks based on most market participants’ incentives, strategies and mandates) are a key part of the alpha generation. An elite compounder specialist doesn’t rely on trading in and out of different companies frequently, but they will be structured to size positions flexibly and to take advantage of volatility to build positions in their highest-conviction ideas.

To illustrate, let’s briefly consider three companies, two of which were mentioned earlier – ADP, Alphabet, and UnitedHealth – through this lens:

- ADP (Automatic Data Processing): Founded in 1949, ADP turned what might seem a mundane back-office task (payroll processing) into a high-moat service. Software companies can have strong competitive advantages through developing products that address critical workflows and make users more productive, leading to stickiness and switching costs. But strongest competitive advantages are found when a software company also has opportunities to meaningfully expand the offering in terms of products and geographies, with leadership that proves adept at executing on these opportunities consistently over time. ADP’s competitive advantages have included (at least for the last 50+ years) scale, decades of proprietary data, and almost tribal knowledge of the various legal and regulatory requirements in key areas like payroll. ADP’s services have been viewed as mission-critical (employees must be paid correctly and on time), creating sticky client relationships – once a company outsources to ADP, switching to another provider has been viewed as risky, inefficient, and costly. And ADP expanded into broader human capital management and benefits administration, increasing its share of clients’ wallets and allowing for longer runways for growth. The combination of these elements that next Fortune 100s possess allowed ADP’s stock to compound at a double-digits pace over the last 60 years post IPO (e.g., not nearly all of this was “priced-in” over most of its public market history), driven by ADP’s ability to grow its free cash flow per share 10%+ annualized over its 60-year post IPO period.

- Alphabet (Google): Google defined the modern era’s data-driven network effect. Its search engine gets more efficient with more usage (more queries improve the algorithm), forming a near-monopoly in search market share. It then smartly monetized this via an auction-based advertising model with virtually infinite scalability. Google’s competitive edge was not only its search algorithm, but also its culture of innovation and long-term thinking (incubated by its founder-CEOs). The company famously states as an operating principle: “focus on the user and all else will follow.” By consistently improving user experience (faster, more relevant search results, free services like Maps, Gmail, Android OS), Google entrenched itself further, yielding more data and more user loyalty – a virtuous cycle. The compounder mindset saw Google as more than a one-trick pony; it saw a platform for organizing information. Indeed, Alphabet today is a conglomerate of Search, YouTube, Cloud services, and “Other Bets” like Waymo (self-driving cars). Through it all, it has maintained high returns on capital and profit margins. From its IPO in 2004 to 2025, Alphabet’s stock produced tremendous total returns (roughly 20%+ annualized, far outpacing the market, again not nearly all was “priced-in”), which only patient, disciplined owners fully captured. There were multiple mispricing moments – for example, when growth temporarily slowed in 2012 or during regulatory scares in 2018 – where the specialist could add to the position, seeing the long-run trajectory was intact (as Google’s core search advertising was still growing and incredibly profitable).

- UnitedHealth Group (UNH): Often overshadowed in headlines by flashier tech companies, UnitedHealth has quietly been one of the best-performing large-cap stocks of the past few decades. In the 1990s, UNH was a regional health insurer; today it’s the largest healthcare company in the U.S. by revenue, with a market cap in the hundreds of billions. How did it compound so successfully? UnitedHealth built a two-pronged moat: its insurance arm (UnitedHealthcare) has network effects and gained scale to spread risk and negotiate favorable rates, while its health services arm (Optum) became a leader in primary care delivery, specialty care, pharmacy benefits, and healthcare IT and analytics. This vertical integration meant UNH could internalize more of the value chain while being better positioned to deliver better outcomes for patients and physicians – an Optum clinic could directly coordinate with the insurance side, using data to improve outcomes and reduce cost. Competitors who lack these pieces are at a disadvantage. UNH’s competitive advantage has grown over time as it amassed more data on patient outcomes and treatment efficacy, feeding into better pricing and services. Essentially, it created a feedback loop much like a tech company, but in healthcare. From an investor perspective, UnitedHealth delivered about a 100-fold increase in share price from the early 1990s to mid 2020s, a great result for a “blue chip” type company that had “thousands of eyeballs on it” – and one earned by those who recognized its unique positioning and had the stomach to stay involved through many bouts of turbulence. Almost regularly, politics (e.g. fears of Obamacare, “Medicare for All” proposals), regulatory changes, and legal investigations have hit the stock, but each time UnitedHealth adapted and continued to grow. An elite compounder specialist can see through this type and level of noise that can be very difficult to stomach by understanding UNH’s fundamental role in the healthcare system and maintaining conviction that this role would only expand with an aging population and the need for more efficiency in U.S. healthcare.

These examples underscore that the companies fitting the elite compounder specialty are often hiding in plain sight. They may operate in any industry and can be headquartered in any country, but they share the traits of strongest competitive advantages, large and growing addressable markets, and management excellence. But to be in a position to repeatedly filter these businesses the right way, and to understand the types of mispricing events that commonly surface around them, you need the same 30,000+ hours of focus and intensity of only studying these dynamics across sectors and geographies as you might see directed towards one sector or geography for those who are commonly labeled as specialists today. For each of these businesses, specialists within their respective sectors can go miles deep trying to learn all the technological know-how in the case of a Google or going state-to-state trying to pinpoint Medicaid patient enrollments in the case of a UnitedHealth. But for these types of companies, we find time and again that the core thesis boils down to no more than a few key factors that do not require a sector-specific background. The required expertise and discipline ends up being just as narrow – perhaps even more so – than those of the commonly accepted specialists despite the fact that the elite compounder specialist develops the required skills through placing much more emphasis on factors that are not sector-specific and instead offer insights into various business types, located in various places, and of various sizes. The elite compounder specialty lies in filtering the signal from the noise – to identify, out of thousands of public companies that could qualify and the hundreds that typically screen well financially at any given time, those few that are best positioned to compound at high rates for many years. This requires intense selectivity (saying “no” to many good-but-not-great businesses, including when they are objectively “cheap” and could provide above market returns over a shorter period), a forward-looking vision of where a company could evolve based on what is in place today, often a contrarian streak, and unusual emotional and mental fortitude paired with avoiding stubbornness to stick with long-term winners even when they look like losers while also acknowledging mistakes and changes in the facts when appropriate.

The securities discussed are mentioned solely for illustrative purposes. They are not designed to represent current holdings of Denmark Capital, which are subject to change without notice, and should not be relied upon as indicative of portfolio composition.

Why This Specialization Has Been Overlooked – and Why It Matters Now

If investing in this type of business is so compelling, why hasn’t the ability to do it effectively and repeatedly been classified as a specialty? There are a few reasons:

- Classification Inertia: The investment industry loves neat categories (large-cap growth, small-cap value, biotech, etc.). A strategy that cuts across sectors and geographies confounds the usual buckets. An investor who owns Toll Brothers, Starbucks, and Tencent in one portfolio – not because they’re in the same sector but because each is viewed as meeting the rigid criteria of an elite compounder – doesn’t fit neatly into style boxes like “tech fund” or “emerging markets.” Many allocators currently misclassify investors who do not fit neatly into one of these categories as “unconstrained, global growth generalists” and assume a lack of specialization. In reality, the specialization is hidden in the criteria being applied, not the location or sector of holdings. It’s easier for a consultant or database to slot managers by simple metrics (sector, market cap focus) than by something as qualitative as “ability to identify strongest competitive advantages.” As a result, few investment RFPs explicitly ask for an “elite compounder” strategy, even though in hindsight that is exactly what produced most of the great track records.

- Short-Term Performance Focus: Backing elite compounders requires patience and often looks downright inefficient in the short run. An investor who often holds stocks for 5+ years will inevitably go through periods of underperformance. Without the right understanding, allocators might fault the manager for being “too concentrated” or “not doing enough” during a quarter or even 3-year period of underperformance. Doing less is often the right move with the right business – let the business compound. The old guard mentality of frequent reporting and quarterly scorecards can be antithetical to this style, unless the allocator is truly aligned with the long-term thesis. It takes a certain kind of investor (often high net worth individuals, family offices, endowments, or visionary RIAs or institutional CIOs) to intentionally seek out this specialty and give it the runway it needs. The good news is that awareness is rising. Most institutions ask managers (of all types) about active share, holding periods, and the sources of their returns. When there’s been unusually strong performance, those questions often reveal that a handful of holdings drove results – which circles back to why identifying those is the paramount skill.

- Misconception of Risk: Some may view a concentrated elite compounder portfolio as higher risk because of less diversification and high volatility. In practice, volatility doesn’t matter if “your favorite holding period is forever,” and diversification isn’t helpful for returns or risk if you are concentrated in the right businesses and define risk in terms of permanent loss of capital risk over time rather than volatility risk. The real risk in markets is often owning a bunch of mediocre businesses that slowly erode value (or don’t go anywhere). By contrast, owning a select set of unusually well positioned businesses can reduce fundamental risk, even if price volatility is higher. Bessembinder’s findings support this: a broadly diversified index works largely because it captures the few big winners, while offsetting the many losers. The elite compounder specialist just tilts that concept to an extreme – focusing only on the winners. Of course, one must be consistently right about them and have processes in place that are effective in mitigating the inevitable mistakes; hence the need for specialized skill and process in these areas, just as specialized skill is required in the areas of commonly defined specialty today like semiconductors, healthcare, or emerging markets. But when executed well, the outcomes have been strong risk-adjusted returns with much lower incidence of long-term capital loss. ADP, Alphabet, and UnitedHealth, for example, all experienced significant drawdowns but eventually rose to new highs on the back of strong business performance; their businesses were ultimately resilient over long periods and less volatile than their respective stocks.

- Prevalence of Look-Alikes and Difficulties in Verifying the True Specialists: It is more difficult for those determining whether an approach constitutes a specialty to vote that way when it involves subject matter they are very familiar with and when so many can sound the part. Anyone who has thought about businesses or been involved with them knows about the importance of having a strong value proposition and competitive advantages. So many fundamentally driven investors today have studied the likes of Graham, Buffett, Munger, Fisher, Lynch, etc. and communicate that their approaches and processes involve filtering for companies that are well positioned in these areas. When it’s familiar terrain with what feels like loads of people communicating similar messages, it can be easy to assume that none can possess specialist or rare expert status within that area.

- The Need for Style-Box Strategies to Hit Asset Allocation Targets and Avoid Overlap: Allocators are investors, too, who are extremely passionate about their work, their missions, and the value they add. As part of this, allocators often establish their own world views, and then allocate capital based on these world views. It can feel that the best way to accomplish this is to allocate to specialists that best fit within the current world view. For example, if the world view is that inflation and rates are coming down, perhaps allocate more heavily to a manager that specializes in high-growth tech stocks. Or if the world view is that valuations are too low in emerging markets, perhaps allocate to those only investing in emerging markets. Investors that specialize in identifying best opportunities under their framework in a completely unconstrained way, who are structured to achieve the strongest returns they are capable of delivering with maximum duration and across different types of market environments, are often at odds with allocators’ desires to express their world views. So the tendency, particularly during a period when public equity benchmark returns have been strong, can be to go “passive” for broad public market exposure and to utilize only those specialists that are narrow enough to allow allocators to express certain elements of their current world views while also allowing them to limit overlap across the allocators’ multi-manager approach.

Now, why is the elite compounder specialty particularly relevant today? In 2026, we are in an environment of technological disruption (e.g., GenAI), which continues to create opportunities for growth and compounding. A faster pace of innovation generally provides more opportunities for more companies to grow their respective free cash flow per share at higher rates for longer. And strong free cash flow per share growth drives share prices over the long-term. We continue to expect a low percentage of companies overall to grow free cash flow per share at double-digit rates over multi-decade periods post-IPO, but a faster pace of innovation is generally conducive to this low percentage nudging a bit higher rather than lower. These dynamics suggest to us that the opportunities for satisfactory returns in public markets over the long-term remain intact, but also that the skew of returns Bessembinder documented will generally persist. In other words, we believe future wealth creation is likely to remain concentrated in a small group of elite compounders, and that the faster pace of innovation makes it more likely that next Fortune 100s will continue to come into the fold.

At the same time, the structure of public markets has caused the world to lose focus on the very specialists who should be best positioned to take advantage of this opportunity for four main reasons that we’ve touched on. First, the prevalence of passive investing has risen dramatically (index funds now hold a large portion of equity assets). Paradoxically, this makes the active pursuit of outliers more valuable, not less. Index funds by design hold everything, including all the wealth-destroyers; they will get the NVIDIAs and Amazons, but also the Enrons, Kodaks, and RadioShacks. And they will hold certain companies in large size that might not be well positioned for strong future performance (and vice versa). The shift to passive moves more flows away from elite compounder specialists but puts these specialists in a better position to outperform by doing more of the same: aiming to avoid the weaker businesses and concentrate in the elites. This is supported by the active / passive debate nuance: Bessembinder’s study gave ammunition to both sides – passive is justified for most, but he also noted “the extraordinary rewards for the active fund manager who invests in these moonshots” with skill and patience. Our view aligns with this: if you can repeatedly identify and stick with the elite compounders (and mostly avoid the landmines), you don’t need to beat the market every month or even every three years – you win over the long-term by capturing the rare companies that compound over long periods. Second, an even smaller percentage of investable assets today has the stomach for true volatility and real down years, which has led to more quant, non-thinking strategies and more “fundamental” strategies with volatility smoothing components that dilute long-term returns and cause many of the decisions to be made for reasons other than views around a company’s current price as compared to its intrinsic value.

These dynamics have allowed strategies and approaches like multi-strategy, market neutral long-short strategies, and quant strategies designed for “no down years” to proliferate, even if they mainly target what we’d consider to be a lower level of net returns. Strategies from elite compounder specialists, on the other hand, that embrace volatility and real down years have only become less in vogue. Third, the qualitative components like competitive advantage that the elite compounder specialist builds skill in over time have high general awareness among allocators and therefore lack “punch” or a “hook” when engaged in discussions, as compared to discussions with, for example, quants who are trying to describe complex algos or semiconductor analysts sharing deep supply chain analysis that can quickly allow the listeners to feel like they are speaking with a “true expert”. And fourth, it is naturally harder for outsiders to gain comfort that they have identified skilled elite compounder specialists because the specialty is rooted in better understanding certain qualitative components that are almost too easy for the 95%+ who claim to possess the specialty but actually do not to look and sound the part, only to underperform over the long-run. The bottom line is several dynamics have come together to drive more of those who could become skilled in this area away and therefore lessen competition at a time when the elite compounder specialist should be strongly positioned.

Conclusion: The Hidden Elite Compounder Specialty is Real and Important

Not all specialties are created equal. Focusing on a particular region or sector may provide an analytical edge around certain companies within those areas, but focusing on elite compounders across industries and geographies, with the right structure that allows for this pursuit in an unconstrained manner, provides a bigger opportunity to express analytical, behavioral, and structural edge around the full set of companies that have driven all the value in public markets over time. Over the last hundred years, specialists in finding the 2-4% of stocks that drove 100% of the gains have effectively harnessed the most powerful force in markets: long-term compounding of extraordinary businesses. This approach has delivered superior returns, with the added benefit of longevity – a portfolio of great businesses can compound for decades, outliving market cycles, whereas many niche strategies tend to shine for a period and then fizzle out when their corner of the market mean-reverts.

But achieving skill in this specialty is far from easy. There is much more nuance to understanding critical components like wow customer experiences, strongest competitive advantages, multi-product opportunities, special governance, and mispricing events than is currently appreciated. And it requires much more experience and far more reps across multiple business models, industries, market environments, and unexpected company-specific situations than is currently appreciated.

Investors must establish a real area of expertise to win – but it’s important to be open-minded about what constitutes a specialty. The traditional labels might blind us to one of the most important specialties of all: the ability to pick long-term winners. Many investors proudly say they only back specialists. Perhaps this memo can help expand that definition.

In practical terms, this means we need more seats at the table for investors who demonstrate: a clearly defined philosophy of quality over quantity, a concentrated portfolio with high active share, a systematic process for position inclusion and sizing, a track record that can be traced to relatively few big stock picks that paid off over time, and the discipline to forever manage a relatively low level of assets to maintain the required flexibility. It also means structuring capital commitments to allow these managers to do their work and avoid shoulder taps during periods of volatility and underperformance (e.g. evaluating performance over 5+ year periods, not monthly or annually). The evidence presented – from Bessembinder’s data to the examples of ADP, Alphabet, and UnitedHealth – shows that this approach is not theoretical but has been the engine behind some of the greatest investment success stories.

In a world where the next Alphabet or Amazon can emerge and create hundreds of billions in value, having a specialist who knows how to identify and nurture those investments is important. It is a different kind of specialization – one that transcends sectors – but it demands at least as much skill and dedication as any traditional niche. In fact, one could argue it demands more: it requires synthesizing knowledge across industries, judging intangibles like management quality, and resisting the herd’s short-term thinking.

To circle back to where we started: markets are largely efficient for the average stock. But for truly elite compounders, markets often undervalue the magnitude and duration of their success, with various mispricing events typically surfacing along the way. The repeated mispricing events are the playground for this specialty. Our view is that the elite compounder specialist is an alpha generator of the highest order – and one whose approach offers a repeatable, enduring edge that cuts across analytical, behavioral, and structural components. It is time to recognize this not as a commoditized or over-populated area, but as a disciplined investment specialty in its own right that has only become less competitive. We believe those who understand this will be better equipped to back investors who can deliver with unusual duration. And investors who practice and believe they have demonstrated skill in this craft should communicate it proudly as their specialty, backed by the evidence we have discussed.

In the end, the most important question for any investor should be: can you capture the wealth created by the very few extraordinary companies? The old guard of the industry, with decades of experience, can surely appreciate that while styles and fads come and go, owning special businesses during periods of mispricing is a strategy that has stood the test of time, yet has remarkably become less populated while most of the daily active trading volume in public markets has shifted towards non-thinking strategies. It’s not easy – nothing in markets is – but it’s simple in concept and profound in outcome. As stewards of capital, embracing this most important specialty could make the difference between average and differentiated performance in the years ahead.

Important Legal Disclaimer & Disclosures

For Informational Purposes Only. This document is intended solely for informational purposes and does not constitute an offer to sell or a solicitation of an offer to buy an interest in any investment vehicle managed by DENMARK Capital Management LLC (the “General Partner”). Any such offer or solicitation will be made only by means of a confidential Private Offering Memorandum and only in jurisdictions where permitted by law.

No Investment Advice. The views expressed herein represent the current opinions of Brandon Ladoff and DENMARK Capital as of the date indicated and are based on the General Partner’s analysis of information available at the time. These views are subject to change at any time without notice. Nothing herein constitutes investment, legal, tax, or other advice.

Portfolio Positions. This document discusses specific financial instruments and/or market sectors (e.g., ADP, Alphabet, UnitedHealth). These references are for illustrative purposes only to demonstrate the General Partner’s thoughts and opinions and are not a recommendation to buy or sell any security. The General Partner and its affiliates may currently hold positions in the securities mentioned and may buy or sell such securities at any time without notice.

Forward-Looking Statements. This content contains forward-looking statements. These statements are based on current opinions, expectations, and assumptions that are subject to risks and uncertainties. Actual outcomes could differ materially. There is no guarantee that any trends discussed will continue.