January 30, 2026

The following reflects personal views of the author as of the publication date and is not intended as investment advice or a description of any investment strategy or performance. Opinions may change and should not be relied upon for investment decisions.

Vision & Mission

As many of you know, I left the “large and stable” world of corporate law in 2012 to pursue an investing career at a small, unknown firm at the time. The decision was based on my passion for the work, the structural issues I began to observe in public markets while practicing law, and my comfort in doing the work that I believed could take advantage of these structural issues.

In early 2025, I left what became a “large and stable” investment management firm with >$80 billion in assets under management at peak during my time there. I concluded that it was necessary to start from scratch and pursue the strategy that I incubated while still there to deliver full value.

Our vision is that public markets are both beautiful and broken. Beautiful because they give us full access to an opportunity set that contains many of the world’s strongest businesses. But broken because human behavior and incentives have caused most market participants to think short-term and / or avoid volatility and true conviction. Mix these two together, and we’re still left with beauty, as these dynamics allow us to pursue the work we love while having the ability to grow our capital at high rates with both duration and liquidity.

Our mission is to show that there’s incredible opportunity in public markets, which is a function of expected annualized net returns, the expected duration of those returns, and liquidity profile. We want to show what I’ve experienced firsthand: that, in our view, growing our capital differently does not necessarily require building small armies of analysts led by risk sheet-wielding decision-makers who feel compelled to maximize daily and monthly returns above all else. And to show instead that winning in public markets with longevity is increasingly about small teams or sole practitioners who are highly trained in the art of extreme simplicity that most cannot stomach for very long.

Ethos

We are challengers. On the investing side, we challenge commonly held views around public market efficiency and volatility. We believe public markets have become less efficient over time. And that we might see more inefficiencies around larger, highly liquid companies with lots of “eyeballs” on them than smaller companies. For example, the 1-5-year share price charts of some of the largest companies on the planet like Netflix, Meta, NVIDIA, Oracle, UnitedHealth, and Taiwan Semiconductor do not suggest “fully understood businesses where all information has been priced in and prior consensus scenario probabilities have been amazingly accurate.” Instead, the returns and share price movements of an increasing number of companies tell a story of a market that has become dominated by firms focused on short-term decision-making, volatility smoothing, or tracking benchmarks.

And there are many other common views around investing in public markets and winning firm and team structure that we challenge today. Our ethos is that we should embrace the pursuit and hunt for greatness, and that in public markets, there needs to be far more seats at the table for those with the right ingredients to be disciplined, long-term focused investors.

Recent Events – 4Q 2025

We refer to 4Q 2025 as the “NVIDIA reversal quarter.” In November, NVIDIA shared its quarterly results and outlook, which we described as a “wow” quarter. Its third quarter Datacenter segment revenue grew an almost incomprehensible 66% year-over-year to reach a very high >$200 billion annual run-rate. Commentary was glowing with multiple flavors of “Blackwell sales are off the charts…cloud GPUs are sold out…compute demand keeps accelerating and compounding across training and inference.” Yet the stock ultimately moved lower. This was part of a swift “tech” selloff over a roughly two-week period that was concentrated in “AI winners.” Although NVIDIA’s share price swing and the tech selloff that occurred around it were confusing at first glance, AI-related skepticism had started brewing for a few reasons:

First, in September-October 2025, multiple non-normal AI-related deals and transactions were announced. For example, OpenAI announced plans to purchase $300 billion in compute from Oracle’s new data center business over the next several years. Oracle’s data centers use NVIDIA chips. NVIDIA then announced that it planned to invest up to $100 billion in OpenAI. Within a short period, OpenAI announced tens of gigawatts of planned data center infrastructure, financed in part by non-traditional arrangements. This naturally led to more questions about whether the pacing and magnitude of the AI infra buildout were appropriate.

Second, in September and October, several high-profile founders and CEOs from companies like NVIDIA, Broadcom, OpenAI, Microsoft, Google, and Meta went on podcast tours and bombarded the market with salesy press releases that mostly described lofty ambitions and future deals that they expected to materialize if the music kept playing. For example, Microsoft CTO Kevin Scott did a Stratechery interview; NVIDIA CEO Jensen Huang did a BG2 podcast episode; OpenAI CEO Sam Altman did many things including an a16z podcast episode; and Broadcom CEO Hock Tan appeared with OpenAI’s Sam Altman and Greg Brockman on the OpenAI podcast. The market grew tired of it, at least for a couple of weeks, culminating with many investors sharing views like this:

And third, in late October, Meta released its third quarter earnings and AI-related outlook including its ongoing AI progress and planned AI infrastructure spending. Meta’s AI progress is important because it is one of the heaviest infrastructure spenders. This is a company that “only” had ~$37 billion in capital expenditures (capex) in 2024. This ballooned to over $70 billion in 2025 (with the incremental capex mostly going towards putting AI servers in the ground) and will likely surpass $115 billion in 2026. The company’s 2026 revenue is expected to be $240+ billion, which means ~50 cents of every dollar in sales could go out the door for capex in 2026! While Meta has experienced great success in utilizing AI to improve various aspects of its core Facebook/Instagram/WhatsApp apps business like content and ad ranking / serving and content creation tool improvements (e.g., the core ad revenue growth Meta just delivered in 4Q 2025 and guided for in 2026 is almost hard to believe), much of its AI capex is going towards building frontier large language models (LLMs). Coming into October, it had become clear that Meta’s LLM efforts had stalled after DeepSeek released an open-source model whose efficiency caught almost everyone by surprise. Meta communicated on its October call that it was moving full steam ahead with AI-related infrastructure spending and hiring. But now, given the clear issues that had emerged with its LLM efforts, the market had its first example of a very big capex spender that, at least for a period, was burning material amounts of this cash, only to realize it had to go back to the drawing board and start over.

AI-related capex has been driving GDP growth. It has also been driving the share prices of several multi-billion and trillion-dollar-plus market cap companies like Meta, NVIDIA, Broadcom, Oracle, and Google. Coming back to NVIDIA’s quarter, as the largest AI enabler in the world, the market will naturally hang on each NVIDIA earnings release for the foreseeable future. Now that we are over three years into the GenAI boom, the market has started to look for any sign of a crack. And the market was particularly ready to find one in November due to the fatigue and concern that built up following a slew of non-normal transactions and promotional press releases. Meta’s 3Q earnings report seemed to be all the “confirmation” the market needed of the mounting fears of low ROI AI-related spend. It boiled over around NVIDIA’s earnings release, leading to a couple of weeks of AI-related market anxiety.

So, there was a sharp intra-quarter tech selloff. Several companies from the neoclouds we have been discussing (Oracle, CoreWeave, Nebius, Iren); to fabless semiconductor design companies like NVIDIA and AMD; to semiconductor manufacturers like Taiwan Semi, SK Hynix, and Micron; to hyperscalers like Amazon, Microsoft, and Google; to application developers spending like crazy on AI infra like Meta, all saw their share prices drop 10-40%+ from late September-October. Certain “tech” companies in other areas like ecommerce also got caught up in the drawdown (e.g., DoorDash). Sentiment can change quickly in public markets, and in this case, it was particularly quick and punishing across most businesses that have been viewed as “AI winners” over the past 1-3 years.

But this type of quick and dramatic psychological shift isn’t uncommon with technological breakthroughs. There is initially excitement or euphoria about the level of economic progress the latest technological breakthrough could unlock, followed by a rush of capital invested to push the pace at which this economic value could be unlocked, followed by some early product successes that demonstrate the possibilities, followed by a slowdown in incremental improvements. Prior to even arriving at the slowdown in incremental progress phase, the market typically starts searching for cracks. For truly breakthrough technologies though, periods of inevitable incremental slowdowns (that are typically met with market drawdowns) are eventually followed by extended periods of incredible product development and innovation that does, in fact, lead to huge productivity gains across broad segments of the population and across many industries.

Currently, we believe we are in that post-euphoria phase where significant long-term excitement for GenAI and its potential (especially agentic workflows) still does, and should, exist. This next phase involves the market becoming more discerning and demanding of clear and far-reaching GenAI product wins before accepting the continued breakneck pace of AI-related spending that involves companies like Meta going from $30 billion-plus in capex in 2022 to likely over $115 billion in 2026. In this next phase, the great innovation we have witnessed starts to bring great questions. The market asks, just how big is this? And what is the pacing and magnitude of further improvements from here? There can be periods of flat out market frustration or even panic if the pace of innovation slows without a clear line of sight into how leading companies and innovators within the industry will be able to develop products / applications that can be used by billions of people in totality, across their personal and work lives, to become much more productive people. In this case, we believe the market is looking for a line of sight into not only when we will get the 10x software engineer (which has already arrived with incredible code generation tools like Codex, GitHub Copilot, and Claude Code), but also the 10x customer service agent, financial analyst, attorney, doctor, film producer, accountant, teacher, local business owner, etc. This will require more advanced GenAI agents that can be used across multiple industries and job types, and it will require that these AI agents are easy and cheap enough to buy and implement that knowledge workers and companies from large to small around the world find themselves getting to a “quick yes” when demoing these tools.

Inevitably, there will be plenty of volatility and market confusion as we progress through these phases. Navigating the rough terrain requires deep conviction in what you own, staying disciplined on what you pay, and having a structure that avoids taps on the shoulder when market narratives that you believe are misguided cause some stocks you own to move against you. In the fourth quarter, starting in late September-October, the market simply started believing (if only for a couple of weeks), “Ok, this might be too much, too fast.” We suspect this question will be asked on multiple occasions going forward.

Where Are We Now? Is SaaS Dead? Is Ecommerce Almost Dead? Will AI Infra Continue to Boom After All?

As we move into 2026, we believe the market has long-term conviction in economic growth and innovation but is suffering from shorter-term confusion. Longer-term positive sentiment around AI, the productivity gains it can unlock, and the long-term opportunities for several companies across the infrastructure and application layers to become much larger over time remain intact. We believe long-term enthusiasm is justified based on what we have seen from frontier models and early GenAI applications like ChatGPT, code-gen tools, full self-driving, and customer service agents. Some of our favorite examples include GitHub Copilot, which is creating nearly 50% of all new code in enterprise environments, Klarna’s AI assistant, which it says is now doing the work of over 850 full-time company agents and handing two-thirds of customer inquiries autonomously, and Harvey, which has allowed several law firms to report saving individual lawyers 8+ hours per week on routine tasks like drafting arguments, deposition prep, and internal memos. And of course, Claude Cowork from Anthropic, which went viral just this month as a non-developer version of Claude Code that brings agentic capabilities like automating workflows to general knowledge work.

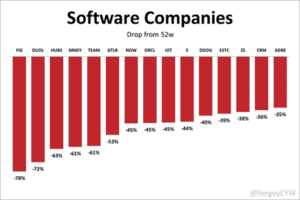

At the same time though, concern and confusion are in the air. There are concerns about market valuations more broadly, and there are concerns around when we will see the type of widespread, clear, and obvious AI progression that would make the market more comfortable with current and planned AI-related capex. For example, a study that went viral in 2025 from MIT’s Project Nanda initiative found that while ~80% of companies have explored GenAI, ~95% of enterprise AI pilots have failed to deliver a measurable financial return or impact the bottom line. Separately, there is also industry-specific confusion. The first industry to take a real hit after internet search (Google) has been enterprise software. Share prices for most have looked something like those shown in the chart below (which has only gotten worse following Microsoft’s and ServiceNow’s earnings releases this week).

We believe enterprise software is a good illustration of how the fast pace of innovation combined with ongoing market structure issues can cut industry valuations massively with almost perfect correlation on the way down. Importantly, innovation, confusion, and powerful narratives can be quite good for idea generation. Even in an environment where valuations are higher more broadly, these dynamics can create more ideas that might generally fall into one of three buckets: (1) Companies fighting powerful narratives related to the new technological breakthrough that we do not currently subscribe to, (2) companies that we believe are both far removed from technological disruption and could actually benefit from it, and (3) companies leading and shaping the technological breakthrough where consensus views might be positive but we believe remain too linear and not positive enough. Today, we’ll share some views on enterprise software, e-commerce, and AI infra to help explain categories #1 and #3.

Is SaaS Dead? Enterprise software (or SaaS) is a good example of how category #1 opportunities can form, although there are certain issues we’re still wrestling with here. There is clearly a powerful negative narrative at work. The market fears (1) GenAI’s code generation capabilities are weakening the moat that certain software companies have enjoyed around building the products (while it’s far from the most important part of the moat certain software companies enjoy, we agree that this aspect is becoming democratized through coding agents), (2) new, AI-first entrants will be better positioned to capture the clearest areas of future growth for the industry, which mostly involves developing and selling AI agents that can either go across systems of record to handle tasks or automate specific workflows within particular apps like Microsoft Office, customer service, or IT service management (we think this is still TBD as it relates to many incumbents), (3) the industry’s seat-based pricing model is doomed because GenAI could at least limit end customer headcount growth but could also lead to significant headcount reductions at end customers (we believe this will be resolved favorably for certain incumbents), (4) easy and cheap access to coding and agents will erase switching costs across the board, even for complex and compliant systems of record with stateful data (we think this is misguided in certain cases), and (5) SaaS management teams do not understand the importance of executing on value-creating M&A and share buybacks (we do not think this is right in all cases). The combination of these fears, along with technical factors like many looking for ways to reduce “tech” exposure in a world where they feel they need more and more semis exposure, has caused ridiculously high correlation across enterprise software stocks, leading to valuations for many like Atlassian, Salesforce, Adobe, HubSpot, and Workday to converge at nearly identical price-to-sales multiples, as shown here:

While we were fortunate in some ways to have come into 2026 with zero direct enterprise software exposure, negative narratives that forcefully takedown entire industries naturally cause us to do more work in the area. And as a side note, this is happening within a market that many are describing as overvalued, serving as a reminder that becoming fixated on higher-level market views can cause you to miss various subplots. For example, companies like Salesforce are growing revenues ~10% annually with what could be expanding margins and are currently valued at ~12x estimated 2027 free cash flow per share. These are the types of mispricing setups that could produce opportunities, and we are prioritizing more than one enterprise software business under our process. However, we should clarify that share price carnage alone does not mean we will find opportunities. It is important to stay mindful of your cost of capital, which should be appropriately high as an equity investor. While we might conclude that low enterprise software valuations already provide a strong margin of safety in certain cases, we also need to see a path to meeting our cost of capital and winning. Under our process, there usually isn’t a path for a company to earn high enough conviction ratings for portfolio inclusion if the conclusion is simply that valuation is low but revenue growth is limited and decelerating with potentially lower free cash flow margins going forward. Miami Heat basketball coach Erik Spoelstra has a saying: “Great players make you watch them.” We are paying particular attention to enterprise software businesses that we believe not only have deeply embedded software solutions with stateful data, but also still have room to grow within their legacy offerings, have a right to win agentic workflows within their areas of expertise, have shown progress towards bringing agents to market that are straightforward to implement and customize, and have excellent management teams that are well positioned to help consolidate the industry while also understanding the importance of returning cash to shareholders when appropriate. Checking all of these boxes would make us “watch”. Most importantly for this discussion, we like to see these types of negative narratives around industries like SaaS because of the opportunities they could produce. And we believe enterprise software is just the tip of the iceberg in terms of AI fears sweeping through different industries over time. As GenAI progresses, it will cover more ground. In fact, literally today, we are seeing AI-related fears sweep across gaming stocks like Roblox after Google announced Project Genie. In the future, further frontier model progression combined with hardware progression could mean that robots become much better surgeons, homebuilders, delivery drivers, etc. This could take decades, but we believe a fast pace of innovation combined with ongoing market structure issues around non-thinking strategies and volatility aversion will lead to sizeable drawdowns related to AI fears across several industries over time. This makes it important to orient the investment process around building long-term conviction and to build a firm structure that is designed to avoid emotional decisions in the face of the increasing number of shoulder taps you are likely to receive from the outside world given these dynamics. Right behind SaaS (and now perhaps gaming and information services), we are seeing the next potential AI-fear-induced victim, which could present a bigger long-term opportunity in our view: Ecommerce.

Is Ecommerce Almost Dead? Ecommerce companies could present another category #1 opportunity. Starting late last year and continuing into 2026, AI-related fears have started bleeding into the ecommerce market. The general market fear is that third party apps like ChatGPT and Gemini will soon provide incredible shopping agents that allow consumers to shop and transact within these apps instead of directly with the Amazons of the world. And if this happens, lucrative components of ecommerce companies’ business models could be in jeopardy like their high margin ads businesses. As a result, the share price performance of many ecommerce companies has been weak since the third quarter. For example, Sea Limited is down ~35% since early October. MercadoLibre is down nearly 20% since late September. Amazon hasn’t moved much in over a year. Coupang is down ~35% since mid-September. Uber is down double-digits since November. And DoorDash is down 25% since early October. These share price declines can be more nuanced and company-specific – for example, DoorDash and Uber fears also include autonomous vehicle (AV) competition; MercadoLibre and Sea fears also include competitive intensity and the lower margins that can come with it; and Coupang fears also include the company’s recent data breach and potential consumer and regulatory fallout as a result – but AI-related shopping agent fears are swirling.

While this could be a period of decelerating revenue growth paired with lower margins for some (which will help determine position sizing), we expect most of these issues to resolve favorably over time. More importantly, the ecommerce companies that are best positioned could represent a different type of opportunity than enterprise software for a few key reasons. First, ecommerce platforms address consumer retail markets that can be in the trillions of dollars as compared to enterprise IT spend that is in the hundreds of billions. For example, US core retail sales are $5 trillion-plus as compared to ~$275 billion for enterprise software, or a difference of >18x. And ecommerce as a percentage of total retail spend across most key geographies remains well below 40%. Unlike enterprise software where a huge focus of corporations is spending on AI-related tools and experimentation, which can and has involved slowing or pausing spend in other areas like more traditional enterprise software, core ecommerce growth rates could remain higher for longer as compared to traditional enterprise software like CRM and human capital management offerings (although spend is not as highly recurring, which the market will likely appreciate again for SaaS one day). Second, certain ecommerce platforms could have clearer paths to adding or continuing with strong product expansion efforts, or “Act II” initiatives. For example, DoorDash has potentially established a right to win in markets beyond the US and in categories beyond restaurant delivery. And Coupang could have interesting opportunities in Korea local services and Taiwan ecommerce. In contrast, we aren’t as clear as of now on how most enterprise software companies we follow will win agentic workloads or how their respective core businesses will evolve alongside agentic workflows. Third, we believe the best positioned ecommerce platforms could be well positioned to “box out” third party shopping agents if they refuse to partner in ways that create win-wins. For example, DoorDash has relationships with hundreds of thousands of local merchants and assists with various functions including merchandising, payments/refunds, and customer service-related work. DoorDash’s network effects across a very fragmented merchant base have allowed it to capture over 50% market share in its core US suburban market. There is high transaction volume within important, everyday categories, which means there are many opportunities for third party shopping agents to make mistakes or provide a weaker user experience in areas that matter to the consumer. For a third-party shopping agent to provide a winning and consistent consumer experience in food delivery, DoorDash could need to cooperate based on its size. This might only happen if the third-party shopping agent served as more of a DoorDash bridge than its own island, and to the extent this would hurt other parts of DoorDash’s business like ads, only if the third-party agent paid licensing or other fees for the right to show these listings.

Based on the narratives that have formed around the ecommerce industry over the last few months, we expect this area to remain fertile ground for idea generation in 2026, but likely with plenty of volatility and potentially with additional share price pain in the near-term.

Will AI Infra Continue to Boom After All? Perhaps the most important component of idea generation and where mispricings are often found is category #3: having higher levels of conviction than others in companies where progress has been mainly smooth and impressive. Valuations for these businesses sometimes “feel” full, but our conclusion is consensus views are not positive enough. In some cases, these companies could be AI enablers. If you are long-term positive on the productivity gains and overall economic value that GenAI will unlock (likely with various bumps along the way), certain companies that are cyclical and capital intensive could present themselves as stronger ideas than you’ve seen in the past. We know from firsthand experience that many investors looking for elite compounders mostly avoid cyclical and capital-intensive businesses, and for good reason historically. After all, all else being equal (which it almost never is), the cyclical, capital intensive business has more risk. Simply put, it is difficult to know whether the cyclical business is over-earning when times are good for operators and investors alike, and there is usually enough competition to push market leaders to invest heavily during the good times to satisfy the higher customer demand that could otherwise go to competitors. What this can lead to is (1) resistance for many investors to size these positions at large weights, (2) a significant lag for many decision-makers (or even a permanent issue for PMs that are more set in their ways) to build the required knowledge base within these previously avoided sectors, and (3) a jumpy market eager to sell when it gets even a whiff of a potential AI slowdown that would hurt these stocks.

We believe it’s important to have penalties for cyclicality and capital intensity, but there are several other factors to consider as well. If other critical factors are unusually strong, there could be an ability for a select few of these businesses to end up clearing the process. More broadly, AI-related breakthroughs and the products it unlocks could translate to new ideas and investments in companies viewed as clear leaders within large and critical areas relating to AI. At the same time, we believe a sound approach to risk management should raise the bar for cyclical businesses and make it very unusual to dive down to #2s and #3s or to niche leaders that operate deeper in the supply chain or where there might be narrower moats like various “neoclouds” in our view.

Before we move on to company-specific discussions, there are, of course, plenty of macro considerations to monitor coming into 2026 like tariffs, inflation and interest rates, unemployment, large government deficits, and geopolitical issues. But we believe healthy GDP growth has a much higher probability of shining through when the pace of innovation is high. It certainly doesn’t hurt that the US government seems to be supportive of doing what it can to help accelerate GDP growth including reducing regulation in important areas like power generation. And we believe that GenAI progress is viewed as so critical to countries’ national security interests that the US push to win here will cause more governments around the world (e.g., China) to adopt pro-growth policies as well. From the laundry list of market concerns coming into 2026, the one we are most focused on is the next-twelve-month progression of enterprise AI agents. We believe it is inevitable that enterprise agents will proliferate across many use cases and allow very large groups of knowledge workers to become much more productive, which should allow certain providers of this software to earn attractive economics. However, the timing is unclear. If the next breakthroughs in this area occur later in 2026 in a way that allows far more enterprise customers to realize they can integrate and customize these agents seamlessly, we believe the probability will only rise from here that current AI-related spending trends will continue over the next ~3 years. Without it though, the likelihood of the type of intense AI skepticism that could lead to a big market drawdown could rise meaningfully. The downside scenario would likely feature several companies like Meta, Salesforce, Workday, etc. providing quarterly results and commentary throughout the year that screams “the AI products we expect to build that will cause our customer engagement to ratchet meaningfully higher are taking longer than expected to come to fruition.”

When the market has this type of long-term conviction but short-term confusion, we believe it is particularly important to understand who you are as an investor, where your investment philosophy is centered, and to have a disciplined investment process that allows you to exercise systematic – but not forced – conviction. We believe an important but overlooked specialty is identifying and backing companies that are well positioned to become next Fortune 100s (or if already there, companies that can become much larger within this group). To be clear, we believe this is a specialty, which we wrote about in our recent Hidden Specialists thought piece. When companies come all the way through a multi-stop process that is built to identify a small group of these types of businesses, today’s market structure likely requires decision-makers that are wired to withstand the behaviorally tortuous exercise of enduring the volatility that will likely hit each of your investments at various points during your holding period in ways that you probably cannot predict ahead of time with any consistency. We strongly believe that enduring volatility is required to perform in public markets over long periods. While we might end up avoiding certain pockets of weakness from time-to-time like the recent enterprise software carnage, we have and undoubtedly will continue to take our share of punches along the way.

So, in this market environment, we continue to execute the process. As it relates to AI, we are staying open to the viewpoint that some of the best businesses for the next 10 years could be more cyclical and capital-intensive than we’ve seen historically, while remaining alert to the risks involved. This environment could also mean that we will stay involved in certain areas that are out of favor and currently classified as “AI losers” if our research continues to conclude that current narratives leading to the share price weakness are misguided. For the companies we are most interested in within e-commerce, their end-to-end control from order to delivery (among other things) has allowed for high market share and sticky customers with habitual purchasing activity. While a weaker consumer and continued investment could potentially limit revenue and/or free cash flow growth in 2026, we have less concern around AI-related disruption for the ones we own and see long tails of growth ahead.

Potential Opportunities

Illumina is a company we have been studying since 2013. Its equipment and consumables are used by research and clinical labs, mainly to sequence the human genome (or parts of it). Its instruments range from its next gen “high-throughput” NovaSeq X (~$1 million per unit) that is designed for high volume sequencing at a low cost per genome, all the way down to its small MiSeq that is built to sequence small portions of the genome. Growth is driven largely by sequencing activity within the installed base and particularly within the high-throughput NovaSeq X units. Clinical customers like diagnostics companies and pharma labs are increasing their sequencing activity levels more than research / academic labs, with the oncology market representing the largest opportunity. Illumina’s clinical customers now represent ~60% of sequencing activity.

Despite addressing an exciting end market and being the clear leader with >65% market share within next gen sequencing instruments and consumables (and higher within whole genome sequencing), the last five years have been nothing short of brutal for Illumina. First, the company was caught up in an antitrust nightmare in both the EU and US after it attempted to acquire a pre-revenue early-stage cancer testing company called Grail (now public) that was actually founded inside Illumina! After absorbing significant operating losses related to Grail while the deal remained in limbo, regulators ultimately forced Illumina to divest Grail for next to nothing. The saga led to an activist campaign, internal strife, and significant leadership changes including a new CEO and CFO. Macro pressures and difficult funding environments in the US and Europe certainly didn’t help and led to tepid demand across the company’s research customers. China (which was ~10% of the company’s revenues at peak) also decided it would move away from Illumina technology and support a local champion instead. New competition from companies like Element and Ultima then surfaced in different segments of Illumina’s business. Lastly, Illumina released its NovaSeq X instrument in 2023, which represented a massive upgrade for customers overall and unlocked the much cheaper $200 genome, but in the near-term, created a big revenue growth headwind because NovaSeq X consumables were priced similarly to the prior generation but allowed for ~2x the sequencing volume. This required customers to sequence ~2x as much to get to breakeven economics versus the prior equipment, which takes time.

The combination of end market pressure, regulatory problems, internal execution missteps, management turnover, China, new competition, and new technology economics broke the stock. And justifiably so, given a lost 5-year period that featured no revenue or free cash flow growth. However, we believe the NovaSeq X platform and the company’s recent progress here have positioned Illumina for continued market leadership. In addition, the end market remains positioned for healthy long-term growth, even if genomics seems like the elephant that never dances. We know there is significant elasticity in genomic sequencing (budget restrictions are real and much of the work can be exploratory in nature), so with the NovaSeq X lowering the cost to sequence the genome by ~50%, we were waiting patiently for confirmation that high-throughput clinical sequencing revenues should inflect higher. If so, Illumina would be well positioned to re-accelerate and grow its total revenues at healthy rates again as more of the business shifted towards clinical customers sequencing on the NovaSeq X. We believe this confirmation was received when the company shared with its third quarter results that clinical consumables sequencing revenue ex China accelerated to 12% year-over-year on the most difficult comparison of the year with ~2/3 of high-throughput clinical sequencing volumes (and growing) now coming from NovaSeq X units.

There is certainly execution risk that remains and a continually evolving competitive landscape to monitor; but with continued progress on the NovaSeq X transition, a clearer opportunity relating to multiomics, integrated software improvements, some green shoots related to China and research budgets, and new management that has been executing well, Illumina could be positioned to regain and maintain its financial strength after a five-year headwind hurricane.

Amphenol is a company that we have missed over the past 10 years – a clear error of omission. This was mainly due to falling victim to a bias that we know exists in public markets and see repeatedly around the companies we look for: a valuation anchoring bias around uniquely durable companies that are currently trading at free cash flow multiples that are above their historical averages but come through the process as being within phases of exceptional growth. These opportunities sometimes surface around unusually strong capital allocators with track records for expanding their respective product portfolios and end market opportunities. Amphenol’s revenue growth accelerated in 2024 but then hit another gear in the back half of 2025 including ~40% organic revenue growth in the third quarter that far surpassed our expectations. We believe Amphenol could have moved into a stronger structural growth position over the past 12 months driven by what management describes as “the revolution in electronics” creating more opportunity and the steps Amphenol has taken to lean into the opportunity. This higher level of revenue growth, coupled with a higher percentage of incremental revenue coming from higher margin products, is allowing for unusually strong free cash flow generation. While this is certainly good for organic growth, there is a double bonus for proven capital allocators that operate in fragmented markets where many firms can run out of steam without access to global distribution and leading customer relationships. This can be seen through Amphenol’s recently completed acquisitions like Rochester Sensors, Trexon, and the large ~$10 billion CCS deal that closed this month.

Amphenol was founded nearly 100 years ago and went public in 1957. ~70 years post IPO, the company’s organic revenue growth is accelerating. Connectors (the plugs, sockets, and interface devices that join electrical or fiber-optic signals between components) are the backbone of Amphenol’s portfolio and account for most of its revenue. These products are typically highly engineered and customized for specific customer applications and help enable the “electronics revolution” across several end markets like automotive, industrial, tech and communications, defense, mobile devices and networks, and commercial aerospace. Of course, the AI-related infrastructure boom has been a big tailwind. But Amphenol’s connectors and interconnect solutions have broad applications and are found in cars, airplanes, factories, telecom infrastructure, data centers, mobile phones, and military systems. As electronics proliferate, the content of connectors and sensors per device or vehicle is rising. For example, latest electric vehicles require 30–40% more connectors per vehicle than traditional cars due to additional high-voltage and data connections. And importantly, as connectivity demands increase within the data center, and as AI-specific architectures become more advanced, Amphenol’s content like high-speed backplanes and connectors can increase by multiples in terms of its percentage of a rack’s bill of materials.

Think product expertise meets consulting expertise to form sticky, trusted customer relationships that put Amphenol in an even stronger position to remain on the “front lines” of more attractive end markets. This helps gain access to the next wave of cutting-edge work for customers, further deepening its trusted relationship status. Organic growth provides more flexibility to pursue the right inorganic opportunities like CCS to allow it to better participate in the quickly rising fiber optic interconnect market (note this should contribute >$4 billion in 2026 sales and be accretive in Year 1). While most deals are far smaller than CCS, there are thousands of connector and component manufacturers globally. Amphenol has proven to be an acquirer of choice, having acquired over 50 companies in the last 10 years alone. These acquisitions bring complementary technologies, new product lines, and customer relationships into the Amphenol fold. The company targets well-managed firms and then retains their leadership (preserving an entrepreneurial culture) while providing global scale and resources.

This is very much an execution-driven business that we believe requires top-notch management. Amphenol is led by CEO Adam Norwitt who has been with the company since the late 1990s. He is widely regarded as a disciplined operator and a champion of the company’s culture. Internally, Norwitt emphasizes an “entrepreneurial organization” with more than 145 general managers worldwide running their units with a high degree of autonomy. This decentralized structure, established by former CEO (now Chairman) Martin Loeffler, has been key to integrating acquisitions smoothly and fostering accountability. Management has a reputation for no-nonsense execution and cost control, often summarized by Amphenol’s cultural tenet of “No Excuses” accountability for results.

While Amphenol’s forward free cash flow per share multiple is currently above its historical average, the market could be underestimating the duration and magnitude of the growth opportunity with an emphasis on the more demanding compute and networking environments of its customers’ solutions leading to more opportunities to add content within server racks and data centers. Areas of strongest growth feature pricing opportunities and high incremental operating margins. Amphenol’s ~100 year history of ruthless focus, discipline and execution meeting unusually interesting end market opportunities should be a nice combination.

The securities discussed are mentioned solely to illustrate our research approach. They do not represent all holdings, are subject to change without notice, and should not be relied upon as indicative of future portfolio composition.

Outlook

In our last memo, we noted that it’s important to stay rooted in your investment approach and philosophy and the overall ethos of your framework, while appreciating that the world can evolve in ways that challenge certain of your prior assumptions. For example, we noted that AI advancements challenge many of our prior assumptions around cyclicality. Today, when you look at the innovation, positioning, and market opportunity for companies like Taiwan Semi (which we have written about at length on multiple occasions and recently became the 6th largest company in the world), it could be harmful to our investment objective to “ding” some of these companies for their cyclicality as much as we have in the past. While we appreciate that “this time” is very rarely different, and that the price to pay for this will likely be increased volatility, keeping a fixed mindset in areas like this could lead to excluding too many best ideas and sizing the ones that clear inclusion thresholds too small.

We also noted in our last letter that political administrations that like to continually wheel and deal can make it more difficult to assess the timeliness of certain opportunities and the magnitude and likelihood of key risks for certain companies. When we wrote this last quarter, the US government and China were actively involved in a high stakes game of (global trade) chicken. That seems to have passed for now. In early January, we added an also short-lived US-Europe squabble to the list. The more movement in these types of areas, the more often our probabilities around big macro risks that wouldn’t be good for how we invest could shift, which could lead to more portfolio activity and turnover than usual.

Despite the added complexities, volatility, and almost constant macro uncertainties, what we do stays consistent at its core. We are dogged hunters for our definition of next Fortune 100 businesses. We narrow to the even smaller group that we believe can grow free cash flow per share in ways that can allow us to exceed our cost of capital. And we aim to only back an even smaller group that falls within one or more of our core mispricing setups. Very importantly, we believe it is important to do it all within a structure that allows for true conviction and challenging the direction that many public market participants have chosen to go.

Sincerely,

/s/ Brandon Ladoff

Brandon P. Ladoff

Founder, CEO & Portfolio Manager

DENMARK Capital

Important Disclosures & Legal Information

For Informational Purposes Only. This document and the information contained herein are provided for informational and educational purposes only. This content does not constitute an offer to sell, or a solicitation of an offer to buy, any security, financial product, or instrument. Any such offer or solicitation would only be made through separate, formal confidential offering documents.

No Investment Advice. The views expressed in this memo represent the personal opinions of Brandon Ladoff and DENMARK Capital as of the date of publication. These views are subject to change at any time without notice. Nothing in this document should be construed as investment, legal, or tax advice. You should consult with your own professional advisors before making any investment decisions.

Disclosure of Interests. The author and/or entities affiliated with DENMARK Capital may have positions in the securities discussed (including, but not limited to, Meta, Taiwan Semiconductor, NVIDIA, Illumina, Amphenol, and DoorDash) and may purchase or sell such securities at any time without notice. The mention of specific securities is solely to illustrate an investment philosophy and research process and should not be viewed as a recommendation to buy or sell.

Forward-Looking Statements. This document contains forward-looking statements based on current expectations and projections about future events. These statements are not guarantees of future performance and involve risks and uncertainties that are difficult to predict. Actual results may differ materially from those expressed or implied.

Risks of Investing. All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Public market volatility can lead to significant price fluctuations that may not align with the fundamental analysis presented here.