When we first started investing professionally, we never thought there could be so much room to evolve our investment process. As outside investors, we believe it is important to start the process with humility. We do not run these businesses day-to-day, and even the best businesses have real risks of business disruption. The world around us can change and can be fragile, and our analyses and judgment are never perfect. As a result, we have always believed a sound investment process that is designed to manage risk effectively should involve considerable time, thought, and documentation. But our thoughts on questions such as exactly what and how to document and what the entire investment process should look like have evolved.

Clearer Objectives and Outcomes

First, we wanted to become clearer on the objectives and outcomes we seek for each company we invest in, along with any metrics that we think should be monitored to help evidence that these outcomes can be realized. These objectives and outcomes can of course evolve over time as we learn more as investors and as the world changes (and as consumer and employee preferences evolve), but the idea is to more clearly lay out what we believe businesses should achieve to earn the long-term trust and engagement of the customers and employees that they were built to serve. Underneath each desired outcome are typically certain metrics or factors (which can also change over time for similar reasons) that we believe can support these outcomes being achieved going forward. Examples today include customer engagement levels, R&D investment, and headcount trends. Our research mostly involves assessing these types of issues from a qualitative perspective, but we have found that being clearer about the outcomes we seek upfront and the metrics that we think evidence that these outcomes are being achieved add discipline and accountability to the process. Particularly for dynamic businesses that might be fairly early in their efforts to serve their potential customers and can have a wider range of possibilities in terms of execution and business performance, these process elements can serve as a check on whether enough patience has been exercised. The goal is to limit bias and avoid big mistakes like being too early or “falling for” intriguing but not truly enduring innovators.

Issues Mapping Exercises

We find another important exercise is mapping out the stakeholder issues that we believe are important to study across customers, employees, and shareholders to determine whether a business has the ability to endure over long periods. We have taken considerable time over the years to think through different stakeholder groups – or the people / groups these businesses were built to serve – and then to map out the issues we feel should be studied to have a view on how well the business is serving these stakeholders and balancing their respective interests.

Before adding these process elements, we studied most of these issues in detail and wrote about them in free form notes; but we lacked an ability to document and better show how this all comes together to inform our conviction rating in a company’s business fundamentals and the investment opportunity overall. This has required more process as compared to relying solely on free form notes for companies of interest that cover many of these same issues; but the payoff can be heightened focus and discipline and an ability to better demonstrate what we believe an enduring business looks like.

Conviction Ratings

We are big believers in the concept of the quantification of a thing bringing more focus to that thing. Specifying the outcomes that we would like every investment in the portfolio to achieve such as leading innovation and attracting and retaining top talent and then thinking through the metrics that help evidence that these outcomes are being achieved in our view, can force us to think a bit harder about whether these outcomes are, in fact, being achieved.

Along the same lines, conviction ratings for both business fundamentals and portfolio selection and sizing decisions can improve focus and decision-making consistency. Yes, internal ratings or scores are as subjective as the qualitative views that inform them. But if you can stay open and realize you don’t need to invest in any particular business, internal conviction ratings can be a nice way to limit bias and confirm that your qualitative views on a company still make sense to you on an absolute and relative basis after translating them to scores and repeating the process across several companies and over time.

For decision-making efforts around portfolio selection and sizing, we utilize a model that includes the factors we consider today across various areas like business fundamentals, variant perception, and portfolio fit considerations. We believe a conviction ratings system for this purpose can serve an important risk management function for portfolio construction and help confirm that portfolio positioning and weights are logical based on our research and qualitative views.

Inevitably, a ton of time is spent within the investment process on factors such as a company’s value proposition, innovation prowess, competitive advantages, addressable market, financial strength, and key risks. But to stay focused on what we are looking for over time, be clear on which companies we ultimately invest in and view as enduring innovators, and be consistent in how the portfolio is constructed, an investment process that includes conviction ratings adds another layer of discipline and decision-making consistency in our view.

Formal Journaling

We have also added formal journaling efforts to our process over the years in an effort to elevate focus and risk management. Journaling is informed by ongoing research. As we update our views and our numbers based on our ongoing research and journaling efforts, we update our portfolio construction model, which connects to portfolio activity. We journal regularly to document company developments, how market prices are changing, and what we think might be implied by these price changes, if anything.

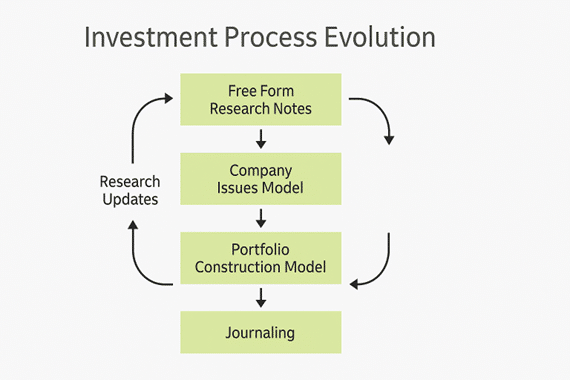

Overall, it is important to elevate the investment process beyond free form research notes and higher-level portfolio selection and sizing decisions. We instead begin with free form research notes, then move to a company issues model that is designed to quantify our qualitative views on a company’s business fundamentals, then move to a portfolio construction model that is designed to quantify our qualitative views on how a company might fit within our portfolio, then move to journaling efforts to continually check our prior views and assumptions. The fundamental company research we do never ends and feeds into these process elements. Our evolved investment process ends up working more like the flowchart below. Our investment process and the way it evolves over time is always designed to bring more focus and discipline to our risk management and decision-making efforts.

Legal Disclaimer

The information herein is not intended to provide, and should not be relied upon for, accounting, legal, or tax advice or investment recommendations. You should consult your tax, legal, accounting or other advisors about the matters discussed herein.

PAST PERFORMANCE IS NOT INDICATIVE OR A GUARANTEE OF FUTURE RESULTS. This document may present past performance data regarding prior/other investments, funds, and/or trading accounts managed by DENMARK Capital Management LLC. This is presented solely for explanatory purposes. The Fund may face risks not previously experienced or anticipated by the General Partner, and therefore, prospective investors should evaluate the Fund on their own merits.

Certain information contained in this document constitutes “forward-looking statements” which can be identified by use of forward-looking terminology such as “may,” “will,” “target,” “should,” “expect,” “attempt,” “anticipate,” “project,” “estimate,” “intend,” “seek,” “continue,” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to the various risks and uncertainties, actual events or results in the actual performance of the fund may differ materially from those reflected or contemplated in such forward-looking statements. DENMARK Capital Management LLC is the source for all graphs and charts, unless otherwise noted.

This document may also present “sample holdings” or “case studies” of a type of asset(s) the fund may invest in or are expected to be typical of its holdings. Such “sample holdings” are not currently holdings of the fund and are presented solely for explanatory purposes.