October 20, 2025

The following reflects personal views of the author as of the publication date and is not intended as investment advice or a description of any investment strategy or performance. Opinions may change and should not be relied upon for investment decisions.

Vision & Mission

As many of you know, I left the “stable” world of corporate law in 2012 to pursue an investing career at a small, unknown firm at the time. The decision was based on my passion for the work, the structural issues I began to observe in public markets while practicing law, and my comfort in doing the work that I believed could take advantage of these structural issues.

In April of this year, I left what became a large and “stable” investment management firm that grew to >$80 billion in assets under management at peak during my time there. I concluded that it was necessary to start from scratch and pursue the strategy that I incubated while still there to deliver full value.

So, at DENMARK, here we are again: shifting from an established position to a challenger seat. Those closest to me know this is where I’m most comfortable based on my upbringing and life experiences. At my prior firm, we were required to take various personality tests before becoming a portfolio manager like the “Enneagram” test. Most reviewed their results with at least some dismay. My results felt obvious to me and others. I’ve had the same mindset for as long as I can remember. Find passions where you can demonstrate skill. Don’t let anyone outwork you on the path to improvement. And don’t be afraid to evolve and challenge the status quo when you believe it is required after careful consideration.

Our vision is that public markets are both beautiful and broken. Beautiful because they give us full access to an opportunity set that contains many of the world’s strongest businesses. But broken because human behavior and incentives have caused most market participants to think short-term and/or avoid volatility and true conviction. Mix these two together, and we’re still left with beauty, as these dynamics allow us to pursue the work we love while having an ability to grow our capital with both duration and liquidity.

Our mission is to show that there’s incredible opportunity in public markets, which is a function of expected annualized net returns, the expected duration of those returns, and liquidity profile. We want to show what I’ve experienced firsthand: that, in our view, growing capital differently does not necessarily require building small armies of analysts led by risk sheet-wielding decision-makers who feel compelled to maximize daily and monthly returns above all else. And to show instead that winning in public markets with longevity is increasingly about small teams or sole practitioners who are highly trained in the art of extreme simplicity that most cannot stomach for very long.

Ethos

As a new firm, DENMARK is often called an “emerging manager.” Yes, we are a new firm that is quite small by industry standards and as compared to the firm that I left. But a major factor as I contemplated this was a realization that commonly held views around the benefits of firm size and “resources” had become stale for what we do.

A friend in the industry recently noted that the term “emerging manager” is outdated and should be replaced with “challenger.” This is our ethos. We are challengers. While our firm and business are emerging, our understanding of the industry and our approach to risk management, investment philosophy, process, and portfolio construction are not.

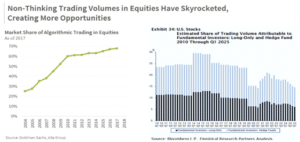

On the investing side, we challenge commonly held views around public market efficiency and volatility. We believe public markets have become less efficient over time. And that we might see more inefficiencies around larger, highly liquid companies with lots of “eyeballs” on them than smaller companies. For example, the 1-5-year share price charts of some of the largest companies on the planet like Netflix, Meta, NVIDIA, Oracle, and Taiwan Semiconductor do not suggest “fully understood businesses where all information has been priced in and prior consensus scenario probabilities have been amazingly accurate.”

Instead, the returns and share price movements of an increasing number of companies tell a story of a market that has become dominated by firms focused on short-term decision-making, volatility smoothing, or tracking benchmarks.

Consider a scenario where an objective research process would conclude that Company A has higher expected returns than Company B over the next 10 years but is more at risk of short-term share price turbulence than Company B. It might look like this:

| Expected 5-Year Revenue Growth CAGR | Expected 1 Year Revenue Growth | Expected Operating Margins | Forward EBITDA Multiple | Return on Invested Capital | |

| Company A | 20% | 14% | 35% | 18x | 25% |

| Company B | 7% | 7% | 15% | 18x | 10% |

Company A is better positioned long-term yet is valued at the same EBITDA multiple as Company B. But now let’s assume that Company A has a digital advertising model, and it’s becoming clearer via alternative data that the economy is softening. This could cause Company A’s revenue growth to dip from 20% to 14% temporarily while Company B’s revenue growth remains steady at 7%. In today’s market, most shares traded daily are handled by those trying to get ahead of this type of short-term slowdown. They often choose to “rotate” into companies whose share prices might be better positioned to perform right now like Company B. We believe these types of dynamics can create opportunities for long-term investors willing to carefully think through intrinsic value and tolerate short-term volatility.

We also challenge the commonly held view that investing passively in public markets is the right choice for those with an ability to do their homework. In our view, passive investing is designed to deliver market-average outcomes, which may or may not align with investors’ objectives depending on their preferences and constraints. In our view, passive investing is unlikely to sustain mid-teens returns over long periods, as benchmark constituents generally grow earnings in the high-single-digit range historically. This means mid-teens benchmark returns for the next 20 years would require higher and higher benchmark valuations. Instead, passive investors should expect returns that are more in-line with underlying benchmark earnings growth, which has been in the 8-10% range over multi-decade periods. Particularly with the cost of capital being higher now, 8-10% does not represent satisfactory returns in our view given the risks you assume as an equity investor.

We appreciate that it’s difficult to find the good apples. And that it’s hard to win. After all, 95%+ of active managers prove to be subpar. But the work we do, just like the work you do, is supposed to be hard. The challenging hunt for the good apples is worth it because compounded returns are powerful. The difference between 10% and 11% annualized returns over 20 years might not sound like much. But as shown below, which is for illustration purposes only, you’d have 20% more capital down the line with that extra one percentage point of performance.

| Value of $1,000,000 compounded at: | Value at Year 20: * |

| 10% for 20 years | $6,727,500 |

| 11% for 20 years | $8,062,312 |

| 13% for 20 years | $11,523,088 |

| 14% for 20 years | $13,743,490 |

*For mathematical illustration purposes only. It does not represent actual or expected performance of any Denmark Capital strategy and is intended solely to demonstrate the mechanics of compound growth.

What about the difference between 10% and 13% annualized returns? Still might not sound like much, but now you’d have 70% more capital with the extra three percentage points of annualized performance. And if you can achieve 14%+ annualized instead of 10%, well now you’d have more than 2x the capital. The world wants us to believe that a “smooth 10%” beats a volatile 13%. But for long-term thinkers with patient capital and emotional fortitude, we do not agree.

Overall, there are many common views around investing in public markets and winning firm and team structure that we challenge today. Our ethos is that we should embrace the pursuit and hunt for greatness, and that in public markets, there needs to be far more seats at the table for those with the right ingredients to be disciplined, long-term focused investors.

Recent Events – 3Q 2025

We would say it was a choppy quarter with a ton of volatility (that has continued into mid-October with fresh US-China tension), but this doesn’t even need to be said at this point. The structure of today’s market fuels volatility. It is something that we believe needs to be accepted and embraced.

Our call outs from the third quarter include the following:

- Global markets were strong, which marked a continuation of second quarter trends. There were several non-normal AI-related deals that fueled the market’s gains. Most of these deals revolve around OpenAI, which has become a force. The flurry of deals, partnerships, and investments were structured as “I’ll pay you if you invest in me” (even if the two sides suggest otherwise), “I’ll pay you if you give me a chunk of your equity,” or “I’ll pay you if you’re willing to stretch your balance sheet to its limits.”

The impact in the third quarter was to drive up share prices massively for some very large companies that we don’t currently own, either due to valuation or business strength concerns. This includes Oracle, Broadcom, AMD and Intel. The most important takeaway for our purposes is that OpenAI has hit a new gear with respect to its product development and investment ambitions. It is led by a talented but very aggressive CEO in Sam Altman who is now going for it all in our view. Note that the recently announced deals came as OpenAI released its second viral consumer app, Sora (ChatGPT was the first). The Sora 2 model it is built on has an incredible mix of design and feel elements including character consistency that creates a much more realistic, emotional, and cinematic AI video generation experience. OpenAI also hosted a developer conference intra-quarter that featured its improved APIs and new ChatGPT functionality like third-party app integration. With 800 million (and growing fast) weekly ChatGPT users, a now viral Sora social media app that opens more revenue opportunities like advertising, leading APIs for third-party integration, and an incredibly talented team that is showing an uncanny ability to innovate across both consumer and enterprise applications, the stage is now set for OpenAI to potentially become a defining company for the next 20 years.

That said, there’s formidable competition and OpenAI’s operations are massively compute-intensive. Altman and his team, along with the company’s board, have considered these dynamics and seemingly concluded that it’s time to go for it all to try and win several massive market opportunities at once. OpenAI has now put a framework in place for over 25 gigawatts (GWs) of compute (figure each GW requires ~$40 billion of spend), which would likely involve building to >$150 billion in company capex by 2030. This makes OpenAI a huge customer for several important companies like Oracle, NVIDIA, and Broadcom. If its revenues scale smoothly over the next 5 years to support these investments, great, everyone can win. But there are plenty of risks involved and the required revenue growth to allow for this massive capex is significant. This creates a high risk, high reward scenario for multiple companies in our view. The market’s attitude towards all of this is currently, “Yes please, I’ll have another.” Although, keep an eye on one of our largest holdings, Taiwan Semiconductor (TSMC). The company, led by veteran CC Wei, has made comments recently that suggest TSMC might not see the world the same way Sam Altman wants them to. Interestingly enough, those that have been running industrial-like companies that are also cyclical – but have run them through many cycles – like CC Wei at TSMC or Jim Burke at Vistra Corp seem to instinctively want to take a more cautious stance than some of those in Silicon Valley who have historically focused on more asset-light business models.

We believe GenAI is, in fact, a massive breakthrough that is still in its infancy and will continually improve to allow for incredible innovation and productivity gains across many industries that we can’t even appreciate today. And we are excited to back companies like TSMC that we believe are the most important driving forces and backbones of the fast pace of innovation we are observing. But we are also aware that there is uncertainty around the pacing and magnitude of these advancements. It’s important to stay mindful of both the quality of what we own and the prices we are paying. A sanity check for us is whether it feels like there are almost endless good investment ideas within a particular area or sector. If yes, there’s probably too much excitement around many of them because there can only be so many special businesses that can withstand the test of time. We like to say that even the best businesses will punch us in the face from time to time if your “favorite holding period is forever.” We want to make sure we only own businesses that we’d feel comfortable adding to during unexpected cyclicality or other non-structural challenges that might send their share prices meaningfully lower.

- More specifically for our portfolio, our companies broadly reported strong calendar second quarter business performance that was reported during the third quarter. This drove several share price “pops” in August, particularly for our largest holdings at the time like Meta and DoorDash. However, the trend was that the share prices of these businesses moved lower over the remainder of the quarter due to a combination of Fed rate cut uncertainty heading into September and headlines that were perceived negatively. For example, headlines suggesting DoorDash could be disrupted by third-party autonomous vehicles (we disagree) and Meta’s apparent setbacks in frontier model building (we agree and trimmed our position meaningfully in the third quarter partly as a result but see plenty of opportunities to mitigate longer-term).

Outside the US, our third quarter returns benefited from holdings such as Tencent and Alibaba that continue to have lower valuations than we’d expect for the level of growth that should lie ahead particularly as business performance has been resilient in key areas like public cloud for Alibaba and advertising for Tencent (although as we write this in mid-October, there are new China-related issues to assess).

Overall, most factors that affect quarterly performance (in both directions) aren’t very meaningful. The one we’d call out as potentially impactful for us is OpenAI’s recent progress in social media. We are closely monitoring how consumers are engaging with AI video generation models like Sora 2 and Veo 3.1, Meta’s ability to respond in a timely manner, and how AI video generation might impact company economics and user behavior on apps like Facebook and Instagram.

- Public market valuations are generally high, particularly in the US, but the global markets we operate within are vast. We have the luxury of picking our spots. While we are not currently seeing the types of rare shots under our framework that can result in 20%+ position sizes (more common during periods of stock market or sector carnage), we continue to have a portfolio of investment opportunities that we are excited about for the next 5+ years at current valuations. This includes certain companies with optically higher valuations like Starbucks, which is currently valued at ~30x our estimate for forward (and in our view very depressed) free cash flow per share, and others like UnitedHealth that are currently valued at low mid-teens multiples on free cash flow per share that we see growing double-digits annualized over long periods.

We do not want to suggest that consistently identifying the right investment opportunities and then sizing them right is easy though, particularly these days when heightened volatility is causing big price changes in both directions within very short periods of time. Plus, macro dynamics like geopolitical swings that could trigger caution under our approach if there is follow-through. For example, just over the past two weeks, we saw an expansion of the China restricted entity list, followed by China’s new rare earth export controls, followed by the US’s new China tariff threats, followed by de-escalation from both sides, followed by re-escalation from both sides, followed by some form of “hopefully we’ll figure it out in a couple of weeks” from both sides. Our portfolio construction model can yield more add / trim activity than normal during periods like this, which generally doesn’t prove to be helpful if the geopolitical risks that are being threatened are ultimately avoided as we’d all hope. In most scenarios though, we aim to stay 90%+ invested in businesses that we are happy to own at current prices and would like to own more of if valuations were to go meaningfully lower.

Sailing to the Right Islands & Cracking the Right Coconuts

Taiwan Semiconductor highlights our risk management perspective and approach to investing in certain companies that are benefiting from GenAI. There’s a delicate balance of sailing to the right islands in an effort to grow capital over time while minimizing the risk of permanent capital loss through backing only companies that we believe have strongest competitive advantages and that we’d be happy to own more of when inevitable challenges surface both operationally and within the company’s end market from time to time.

TSMC has continued to grow its revenue by over 30% in recent quarters on a high base of ~$90bn in 2024 revenues. Guidance calls for continued ~20% revenue growth from here that we believe is conservative based on TSMC’s competitive positioning, the nature of and requirements for leading-edge nodes, and overall end market demand. With even more manufacturing and packaging complexity involved at the leading-edge and 2-3-year lead times that require close partnerships between Taiwan Semi and its customers, it has proven difficult for other fabs like Intel and Samsung to take significant market share. With improvements across multiple dimensions of frontier models like training, reinforcement learning, and inference, the demand for compute and leading-edge chips continue to be difficult for TSMC to keep up with. The volume growth TSMC is experiencing comes with pricing opportunities, which is leading to higher underlying gross margins. In addition, the increasing complexity of these chip designs requires more of Taiwan Semi’s advanced packaging solutions.

At the same time, we admire TSMC’s management and their long history of approaching customer ambitions with both optimism and realism. While it could prove difficult to turn away business from its customers’ customers like OpenAI, TSMC has shown some restraint with respect to its capex plans thus far that seems refreshing during times like this.

As compared to certain other direct AI beneficiaries, we like that (1) Taiwan Semi can lean into this opportunity by continuing to do “more of the same” by advancing its core operations, and (2) as a manufacturing partner for the broader industry, can benefit even if some of its customers who are currently driving end market demand see a change in their competitive positioning while others strengthen. Yes, Taiwan Semi has a different “China risk” as compared to others benefiting from the rise of AI that we have spoken about at length including why we believe common views are misguided that there is meaningful risk of an imminent, overnight China attack or, alternatively, a “peaceful” Taiwan surrender that would occur without a war.

Compare this to another AI beneficiary that we admire in certain ways, Oracle. After continuing to follow closely, we are still choosing to remain on the sidelines with Oracle and other “neoclouds” like Coreweave, Nebius, and Iren. Oracle earns less than $40bn in revenue annually from its core database and other software solutions like ERP. It is now projecting that its newer AI factory or “neocloud” business will grow to an astonishing $165 billion in revenue (or more) by May 2030 (~4.5 years out) from almost $0 a couple of years ago. Much of this is being driven by OpenAI who has a framework in place to ultimately receive $100 billion investment from NVIDIA, the company Oracle is buying most of its GPUs from as part of its Stargate data center buildout with OpenAI. In other words, Oracle is bolting on a new business that has quickly become its most important business and that is being financed through taking on a bunch of debt and indirectly through its large customer entering into non-normal arrangements with interested parties.

In fairness, Oracle deserves a lot of credit for seeing and executing on this opportunity (thus far). Oracle didn’t snatch this opportunity out of thin air. It acquired Sun Microsystems years ago, giving them significant hardware engineering expertise. This helped give the company the know-how to build hardware and AI server racks. It used this know-how to create its Cloud Infrastructure Gen2 that scores well on both performance and cost-efficiency for AI-related workloads.

Still, the company has transformed almost overnight from a highly recurring revenue, software-dominated business with manageable cyclicality, a strong balance sheet, and no real customer concentration to speak of, to a company that is intensely focused on AI infrastructure with very high customer concentration and much higher cyclicality than its traditional software business and that also requires the company to stretch its balance sheet. If, for example, OpenAI stumbles and is unable to ramp its revenues as much or as quickly as planned, Oracle could experience meaningfully more pain in terms of where it lands five years from now versus current expectations than a company like Taiwan Semi that is more agnostic to where AI value creation is coming from.

The bottom line is that it’s important for us to sail to the right islands, but we must also look to crack the right coconuts and do it in a way that fits within our approach to risk management. With situations like Oracle today, we often find ourselves saying we’d rather allocate the next $1 to our best idea even if it’s already a large position for us. This can allow for more conviction in adding to our position when there are inevitably speed bumps within this dynamic and cyclical industry, and in connection with this, it can ultimately lead to better outcomes if our research proves directionally accurate.

Potential Opportunities

Potential opportunities identified in the third quarter include Thermo Fisher Scientific and Repligen.

Thermo Fisher earns most of its revenue from customers in the pharma and biotech industry. Through internal product development efforts and acquisitions, Thermo offers a broad menu of tools and services that can allow it to serve as a “one-stop shop” and foster trusted relationships with its customers. These relationships are built on product quality, convenience, and competitive pricing. While Thermo’s annual revenue has grown to greater than $40 billion over the years, it has been anything but smooth sailing post-Covid. Instead, in areas such as lab products and instruments, outsourced drug manufacturing, and outsourced clinical trial operations, Thermo’s revenue growth has dissipated. Many customers built up inventory during the pandemic that has led to a multi-year destocking cycle including some cases of customers ordering 5-6x normal volumes anticipating shortages. Based on activity levels at the time, Thermo also expanded its drug manufacturing capacity during the pandemic in a way that required time to grow into. Within its sales to academic institutions, product growth in categories like electron microscopy has been affected by funding cuts and policy uncertainty. There have been tariff-related impacts on revenue growth in 2025 particularly within the company’s Analytical Instruments segment. China, which represents approximately 10% of total revenue, has been declining due to tariffs, a weak Chinese economy, and an always tough competitive landscape. For Thermo’s outsourced drug manufacturing business and outsourced clinical trial business, many biotech customers have faced constrained budgets due to economic uncertainty and the weakness many of them have experienced in their own respective businesses post-Covid. Effectively, it has been a “headwind hurricane” for Thermo, many of its peers, and the broader healthcare sector.

When competitively advantaged businesses like Thermo that operate within end markets that have and should again grow 4-6% annually experience business weakness for a prolonged period, we repeatedly see mispricing events surface due to the market’s increasing short-termism. In Thermo’s case, the structural and behavioral issues that we see affecting an increasing number of market participants in these situations can create enough apathy and desire to look elsewhere that valuations can fall to levels that we view as too cheap based on our views of the underlying business and its prospects. We see a business that remains well positioned to take 2-3+ percentage points of market share through its stronger innovation and deeper, stickier customer relationships as compared to peers. CEO Marc Casper and team have also demonstrated excellent stewardship and capital allocation decisions over the years, which we expect to continue to allow for accretive M&A opportunities within many of the company’s fragmented markets. Now that there could be early data points suggesting Thermo is on its way to a gradual recovery of 3-6% organic revenue growth over 2026-2027, Thermo could be more interesting.

Repligen is a much smaller company located right in Thermo’s backyard in Waltham, MA. In fact, several Repligen employees have come over from Thermo. This includes Executive Chairman Tony Hunt who was President of Bioproduction at Life Technologies, which was acquired by Thermo in 2014. Hunt is credited with architecting Repligen’s evolution into a pure-play bioprocessing company that serves perhaps the most attractive end market within Thermo’s more diversified portfolio. Bioprocessors like Repligen (and Thermo) provide equipment and consumables to biopharma companies and contract development manufacturing organizations (CDMOs) that are manufacturing drugs for clinical trial or commercial purposes. Like Thermo but to an even larger extent given its concentration in bioprocessing, Repligen has suffered post-Covid setbacks. Revenue peaked at ~$800 million in 2022, only to fall back to ~$640 million in 2023. Interestingly though, Repligen has used this time to significantly advance its upstream (e.g., growing cell cultures) and downstream (e.g., filtering, processing) biomanufacturing workflow tools. In filtration, which is the cornerstone of the company and its largest franchise, its flagship XCell Alternating Tangential Flow (ATF) systems are now market leading.

Repligen’s ATF systems have enabled the industry to start to move on from fed batch processes to “continuous,” which is more efficient and cost effective for customers. Getting in the door with ATF systems and now having a broader portfolio upstream and downstream can allow Repligen to grow its revenues 5+ percentage points above industry growth rates that have historically been in the 8-12% range. Note that penetrating this market takes time, as customers often have workflows that have already been validated on other equipment. Practically, many customers also want to see the legacy equipment they’ve already purchased fully depreciate before they upgrade. Overall, similar market dynamics to those discussed with Thermo above could be creating a potential investment opportunity with Repligen, plus a potential lag in appreciating the differentiation in Repligen’s product portfolio and how it could drive strong growth for the company in the years ahead.

The securities discussed are mentioned solely to illustrate our research approach. They do not represent all holdings, are subject to change without notice, and should not be relied upon as indicative of future portfolio composition.

Outlook

It’s important to stay rooted in your investment approach and philosophy, which are based on your belief system as an investor and how you approach risk. At the same time though, the world can evolve in unexpected ways, so it’s important to stay open to whether there’s room for certain of your prior assumptions to be challenged without changing the ethos of your framework.

For example, generative AI advancements challenge many of our prior assumptions around cyclicality. All else being equal (which is almost never the case, but let’s just assume it is for a minute), the cyclical business involves more risk than the non-cyclical one for both investors and operators. High cyclicality makes it harder for both investors and operators to understand what normalized demand truly looks like during non-cyclical times and makes it more difficult for investors and operators to understand most effective ways to allocate capital as a result. Today though, when you look at the innovation, positioning, and market opportunity for companies like Taiwan Semi, it could be harmful to our investment objective to “ding” some of these companies for their cyclicality as much as we have in the past. Doing so could lead to excluding too many of them and sizing the ones that meet our conviction ratings threshold too small. In other words, achieving our investment goals could very well require more “volatility pain” along the way if more of the world’s innovation is being driven by more cyclical businesses.

Political administrations that like to continually wheel and deal can also make it more difficult to assess the timeliness of certain opportunities and the magnitude and likelihood of key risks for certain companies. For example, the more high stakes games of (global trade) chicken that certain governments are willing to play with each other, the more often our probabilities around big macro risks that would not be good for how we invest could shift, which could lead to more portfolio activity and turnover than usual.

Despite the added complexities though, what we do stays consistent at its core. We filter for world-leading competitive advantage and large, growing addressable markets. We narrow to the even smaller group that we believe can grow free cash flow per share in ways that can allow us to exceed our cost of capital. And we only back the even smaller group that falls within one of our core mispricing setups. Very importantly, we do it all within a structure that allows us to express true conviction and challenge the direction that most public market participants have chosen to go.

Even during early-to-mid October, market sentiment has shifted from one of excitement and opportunity to potentially one of AI fatigue and renewed geopolitical concern. It has become rare for our portfolio to move by less than 50 basis points per day. We expect our returns to look meaningfully different from the benchmark from month-to-month and year-to-year. But we continue to identify at least a small group of companies that possess the characteristics we look for and exhibit the mispricings we aim to identify in support of our long-term objectives.

Sincerely,

/s/ Brandon Ladoff

Brandon P. Ladoff

Founder, CEO & Portfolio Manager

DENMARK Capital

Important Legal Disclaimer & Disclosures

For Informational Purposes Only. This document is intended solely for informational purposes and does not constitute an offer to sell or a solicitation of an offer to buy an interest in any investment vehicle managed by DENMARK Capital Management LLC (the “General Partner”). Any such offer or solicitation will be made only by means of a confidential Private Offering Memorandum and only in jurisdictions where permitted by law.

No Investment Advice. The views expressed herein represent the current opinions of Brandon Ladoff and DENMARK Capital as of the date indicated and are based on the General Partner’s analysis of information available at the time. These views are subject to change at any time without notice. Nothing herein constitutes investment, legal, tax, or other advice.

Portfolio Positions. This document discusses specific financial instruments and/or market sectors (e.g., TSMC, Oracle, Thermo Fisher, Repligen). These references are for illustrative purposes only to demonstrate the General Partner’s investment process and are not a recommendation to buy or sell any security. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities discussed. The General Partner and its affiliates may currently hold positions in the securities mentioned and may buy or sell such securities at any time without notice.

Forward-Looking Statements. This content contains forward-looking statements. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially. There is no guarantee that any trends discussed will continue.

Performance & Risk. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Investing in public markets involves a high degree of risk, including the risk of the total loss of capital. The mathematical examples regarding compounding rates (e.g., 10% vs 14%) are hypothetical illustrations of mathematical principles and do not represent the performance of any specific fund or strategy.